When All the Costs Add Up

We’ve spent nine parts examining individual cost categories. Banking fees. Credit card debt. Forced car ownership. Food monopolies. Phone and internet. Insurance. Fees everywhere.

Each part showed how one sector shifted costs onto working Americans while profits soared.

Now let’s see what happens when you add them all together.

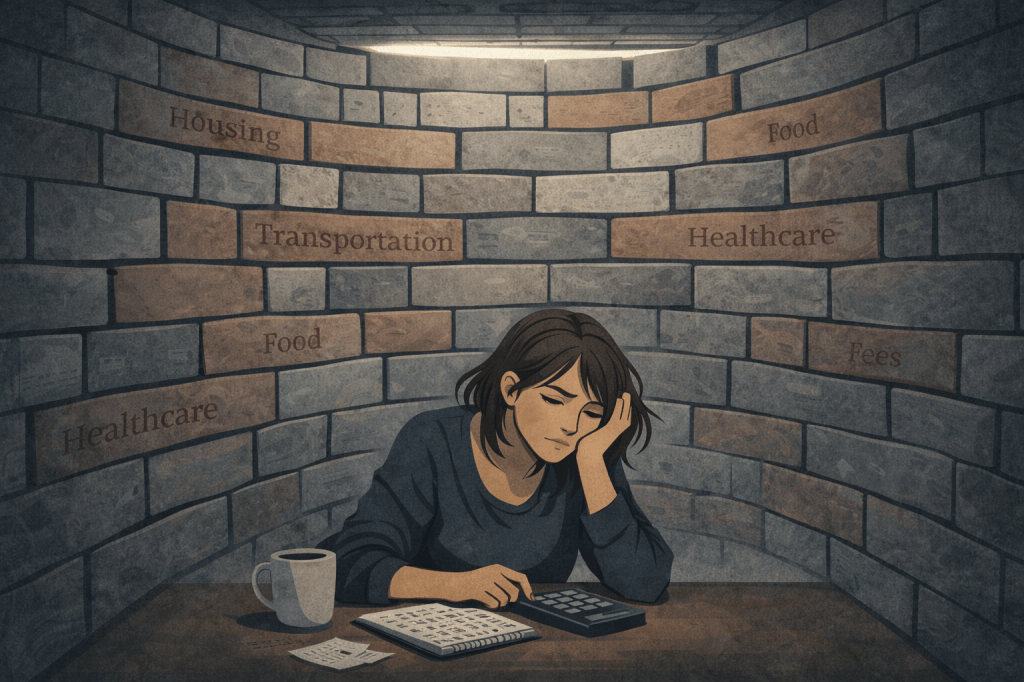

Meet Emma. She’s not real, but she’s based on real numbers. She’s a composite of Sarah, Jason, Jennifer, Maria, Rachel, Lisa, David, and Tom—the people we’ve been following. She represents the median American worker.

Here’s her life in dollars.

Emma’s Profile

Age: 32 Job: Registered nurse at a hospital Income: $77,000/year (above median individual income of $59,228) Location: Mid-sized city, Southeast U.S. Family: Single, no kids Education: Bachelor’s degree, $38,000 in student loans Car: 2019 Honda Civic, financed Housing: Rents a one-bedroom apartment

Emma works hard. She’s responsible. She budgets. She doesn’t live extravagantly. She’s doing everything right.

Let’s do her math.

Emma’s Income Reality

Gross annual income: $77,000

Deductions:

- Federal income tax: $10,267

- FICA (Social Security + Medicare): $5,891

- State income tax: $3,542

- Health insurance (employee portion): $2,400

Take-home pay: $54,900/year ($4,575/month)

That’s what actually hits her bank account. Now let’s see where it goes.

The Mandatory Costs: Every Category

Housing (From Part 1)

- Rent: $1,450/month

- Renters insurance: $15/month

- Subtotal: $1,465/month ($17,580/year)

Transportation (From Part 5)

- Car payment: $350/month

- Auto insurance: $180/month

- Gas: $160/month

- Maintenance/repairs: $92/month

- Registration/fees: $15/month

- Parking at work: $20/month

- Subtotal: $817/month ($9,804/year)

Food (From Part 6)

- Groceries: $380/month

- Eating out/coffee: $70/month

- Subtotal: $450/month ($5,400/year)

Healthcare (From Parts 1 & 8)

- Insurance premium (employee portion): $200/month

- Deductible/co-pays/prescriptions: $150/month (averaged)

- HSA contribution: $125/month (to cover deductible)

- Dental/vision insurance: $50/month

- Subtotal: $525/month ($6,300/year)

Student Loans (From Part 1)

- Monthly payment: $340/month

- Subtotal: $340/month ($4,080/year)

Phone & Internet (From Part 7)

- Internet: $89/month

- Cell phone: $75/month

- Subtotal: $164/month ($1,968/year)

Utilities (From Part 1)

- Electric: $95/month

- Water/sewer/trash: $65/month

- Subtotal: $160/month ($1,920/year)

Banking & Credit (From Parts 3 & 4)

- Credit card interest (on $3,800 balance): $63/month

- Credit card minimum payment (beyond interest): $52/month

- Bank account fees: $12/month

- ATM fees: $6/month

- Subtotal: $133/month ($1,596/year)

Other Mandatory Fees (From Part 9)

- Rent payment convenience fee: $35/month

- Utility payment fees: $8/month

- Subscriptions (streaming – 2 services): $25/month

- Various monthly fees: $15/month

- Subtotal: $83/month ($996/year)

Basic Necessities

- Household items/toiletries: $60/month

- Clothing/shoes: $50/month

- Laundry: $30/month

- Personal care: $45/month

- Subtotal: $185/month ($2,220/year)

Emma’s Monthly Budget

Total Monthly Income (after taxes): $4,575

Total Monthly Mandatory Expenses: $4,322

Remaining: $253/month

What’s NOT in That Budget

Emma has $253/month left. But she still hasn’t paid for:

Savings and Emergency Fund: $0

The experts say you should have 3-6 months of expenses saved. That’s $13,000-26,000. Emma has $1,200 in savings. One car repair or medical emergency away from debt.

Retirement: $0

Her employer offers a 401(k) but no match. Financial advisors say save 15% of income for retirement. That would be $963/month. Emma contributes $0.

Entertainment/Hobbies: $0

- Gym membership: $50/month

- Going out with friends: $80/month

- Movies, concerts, events: $40/month

- Hobbies: $30/month

Total if she did these: $200/month

Gifts and Holidays: $0

- Birthdays: $40/month (averaged)

- Christmas/holidays: $83/month (averaged, $1,000/year)

- Total: $123/month

Vacation: $0

Emma hasn’t taken a real vacation in three years. A modest week-long trip would cost $1,500-2,000. That’s 6-8 months of her $253 surplus.

Unexpected Expenses: $0

- Car repair beyond the $92/month average

- Medical bill beyond the averaged $150/month

- Vet bill (she wants a dog but can’t afford one)

- Home repair (rental, but she pays for some small things)

- Anything breaking (laptop, phone, appliances)

Down Payment for a House: $0

The median home in her city costs $320,000. A 20% down payment is $64,000. At $253/month savings, that would take 253 months (21 years). And that’s only if she never has a single unexpected expense.

The Actual Math

Emma makes $77,000/year—30% above the median individual income.

After all mandatory expenses, she has $3,036/year left over ($253/month).

That’s 5.5% of her take-home pay. For everything else in life.

And remember:

- She’s single (no kids to support)

- She’s healthy (no chronic conditions)

- She has no major debt beyond student loans and a modest car payment

- She lives in a moderate cost-of-living area

- She makes above-median income

If Emma, who is doing everything right and earns more than most people, can barely survive, what about everyone else?

The Median Income Reality

Let’s run the same numbers for someone making the actual median individual income of $59,228.

Take-home pay: $45,000/year ($3,750/month)

Using the same expenses (which are conservative for most cities):

- Housing: $1,465

- Transportation: $817

- Food: $450

- Healthcare: $525

- Student loans: $340

- Phone/Internet: $164

- Utilities: $160

- Banking/Credit: $133

- Fees: $83

- Necessities: $185

Total: $4,322/month

Income: $3,750/month

Shortfall: -$572/month

The median American worker is $572 short every single month before considering:

- Savings

- Retirement

- Entertainment

- Emergencies

- Any quality of life

They’re not making it. The math doesn’t work.

Where the Money Went

In Part 2, we showed that if wages had tracked productivity since 1970, the median worker would make $102,000 instead of $59,228.

That’s a $42,772 gap.

Where did that $42,772 per worker go?

Let’s trace it through our nine parts:

Corporate Profits (All Parts)

Healthcare insurers (Part 8):

- Top 4 combined profit: $43.4 billion (2023)

- Spread across ~160 million insured Americans: $271 per person

Auto insurers (Part 8):

- Industry profit: $42 billion

- Spread across 230 million drivers: $183 per person

Food monopolies (Part 6):

- Tyson, Kroger, Walmart, Cargill combined profit: ~$45 billion

- Spread across 130 million households: $346 per household

Banks (Parts 3 & 4):

- Top 4 profit: $110.9 billion

- Fee revenue: $52 billion from consumers

- Interest revenue: $120 billion from credit cards

- Per household: $1,323

Telecom companies (Part 7):

- Comcast, AT&T, Verizon combined profit: $41 billion

- Per household: $315

Auto manufacturers & finance (Part 5):

- GM, Ford, Stellantis profit: $32.9 billion

- Auto finance profit: $15 billion

- Per car-owning household: $255

Credit card industry (Part 4):

- Interest and fees: $120 billion

- Per household with credit cards: $923

Fee economy (Part 9):

- Total fees: $300 billion

- Per household: $2,308

Total corporate profit from shifted costs: ~$553 billion/year Per household: ~$4,254/year

Executive Compensation

We’ve documented CEO pay throughout this series:

- Ticketmaster CEO: $139 million

- UnitedHealth CEO: $23.5 million

- T-Mobile CEO: $54.4 million

- Comcast CEO: $32.5 million

- Walmart CEO: $26.0 million

- Tyson CEO: $13.7 million

Average S&P 500 CEO compensation (2023): $16.3 million Average worker compensation: $66,600 Ratio: 244:1

In 1970, the ratio was 21:1.

Stock Buybacks and Dividends

Companies spent record amounts buying their own stock instead of investing in workers:

2023 Stock Buybacks (selected companies from our series):

- Comcast: $11.9 billion

- AT&T: $16.1 billion

- Walmart: $9.2 billion

- UnitedHealth: $6.1 billion

These buybacks boost stock prices, which benefits:

- Executives (whose pay is tied to stock price)

- Wealthy shareholders (top 10% own 89% of stocks)

They don’t benefit:

- Workers (whose wages stagnate)

- Customers (whose prices increase)

The Compounding Breakdown

Let’s see exactly how Emma’s $77,000 income gets consumed by all the shifted costs:

Gross Income: $77,000

Taxes (including healthcare):

- Federal, FICA, State: $19,700

- Healthcare insurance (employee portion): $2,400

- Subtotal: $22,100 (28.7% of gross)

Housing (Part 1):

- Rent and insurance: $17,580 (22.8% of gross)

Transportation (Part 5):

- Car, insurance, gas, maintenance: $9,804 (12.7% of gross)

Food (Part 6):

- Groceries and eating out: $5,400 (7.0% of gross)

Healthcare beyond insurance (Parts 1 & 8):

- Deductibles, co-pays, prescriptions: $3,900 (5.1% of gross)

Student Loans (Part 1):

- Monthly payments: $4,080 (5.3% of gross)

Phone & Internet (Part 7):

- Mandatory connectivity: $1,968 (2.6% of gross)

Utilities (Part 1):

- Electric and water: $1,920 (2.5% of gross)

Banking, Credit, Fees (Parts 3, 4, 9):

- Interest, fees, charges: $2,592 (3.4% of gross)

Basic Necessities (Part 1):

- Household items, clothing, personal care: $2,220 (2.9% of gross)

Total Consumed: $71,564 (92.9% of gross income)

Remaining for everything else: $5,436/year (7.1%)

That $5,436 has to cover:

- All entertainment and social life

- All gifts and holidays

- All emergencies

- All unexpected expenses

- All retirement savings

- All other savings

- Any quality of life improvements

And remember: Emma makes $17,772 MORE than the median worker.

The Median Worker’s Impossible Math

For someone making $59,228 (median):

Take-home after taxes: ~$45,000

Same expenses: $67,464 (using Emma’s conservative numbers)

Shortfall: -$22,464/year (-$1,872/month)

They can’t make it without:

- Credit card debt (Part 4): Average $6,501, costs $1,395/year in interest

- Payday loans

- Overdraft fees (Part 3)

- Working second jobs

- Skipping healthcare

- Delaying car maintenance (until catastrophic failure)

- Skipping meals

- Not saving for retirement

This is 50% of American workers.

Half of working Americans are underwater before they even try to save or have any quality of life.

The 1970 Comparison: What Changed

In Part 2, we showed what the 1970s looked like. Let’s compare to Emma:

1970 worker (Robert, the machinist):

- Income: $9,400 ($70,400 in 2024 dollars)

- Housing: 22% of income (bought a house)

- Transportation: 9% of income (two cars, owned)

- Healthcare: 3.6% of income (employer-paid, no deductibles)

- Education: $400/year for kids’ college (4% of income)

- Food: 14% of income

- Savings: 10% of income

- Total: 62.6% of income

- Remaining for quality of life: 37.4%

2024 worker (Emma):

- Income: $77,000 (9% higher than Robert, inflation-adjusted)

- Housing: 22.8% of income (renting, can’t buy)

- Transportation: 12.7% of income (one car, financed)

- Healthcare: 5.1% + 3.1% premiums = 8.2% of income (high deductibles)

- Student loans: 5.3% of income (debt for her own education)

- Food: 7.0% of income

- Phone/Internet: 2.6% (didn’t exist in 1970)

- Credit/Banking/Fees: 3.4% (minimal in 1970)

- Utilities: 2.5%

- Necessities: 2.9%

- Total: 67.5% of income

- Remaining for quality of life: 7.1%

What changed:

- Robert had 37.4% of income for savings, retirement, quality of life

- Emma has 7.1%

- Emma has 30.3 percentage points less disposable income

Robert supported a family of four on one income and saved 10%.

Emma can’t save, can’t buy a house, can’t have kids, on a higher income with no dependents.

The costs shifted. The wages didn’t follow.

The Wealth That Vanished

If Emma made what productivity gains suggest ($102,000 instead of $77,000), she’d have an extra $25,000/year.

That $25,000 would allow her to:

- Max out her 401(k): $7,000/year (employer match would add more)

- Build emergency fund: $5,000/year

- Save for house down payment: $8,000/year (8 years to $64,000)

- Actually have a life: $5,000/year

Instead, that $25,000 went to:

- Corporate profits

- Executive compensation

- Stock buybacks

- Shareholder dividends

She produced the value. They collected the money.

The Tipping Point

Emma is at the tipping point. One bad event pushes her into debt:

Car transmission fails: $3,500

- Emergency fund: $1,200

- Shortfall: $2,300

- Goes on credit card at 21% APR

- Now paying $40/month in interest

- Remaining monthly surplus: $213 (was $253)

Six months later, needs root canal: $1,800

- Emergency fund: Still depleted from car

- Goes on credit card

- Credit card balance now: $6,100

- Interest: $107/month

- Remaining monthly surplus: $146

Medical bill for ER visit: $2,400 (hit her deductible)

- Must be paid within 90 days

- Goes on credit card

- Credit card balance now: $8,500

- Interest: $149/month

- Minimum payment: $255/month

- Monthly shortfall: -$2/month

Emma is now underwater. And she hasn’t done anything wrong. She got sick. Her car broke. Normal life events.

Within one year, she goes from $253/month surplus to -$2/month shortfall.

And the credit card interest means she’s paying back far more than she borrowed:

- $8,500 at 21% APR

- Paying minimums: 18 years to pay off

- Total interest paid: $9,800

- Total paid: $18,300 for $8,500 in expenses

The median worker doesn’t have Emma’s $253 cushion. They start at -$572/month.

The National Picture

130 million households in America

If the median household is short $572/month, that’s:

- $74.4 billion per month in shortfall

- $892.8 billion per year

That’s the total amount Americans are short annually trying to cover basic costs.

Where does that money come from?

- Credit cards: $1.13 trillion in outstanding debt

- Auto loans: $1.63 trillion

- Student loans: $1.77 trillion

- Payday loans: $90 billion annually

- Personal loans: $240 billion

Total household debt (excluding mortgages): $4.9 trillion

Americans owe $4.9 trillion because wages don’t cover costs.

And who profits from that debt?

- Banks charging 21% on credit cards

- Auto finance companies charging 7-11% on car loans

- Student loan servicers

- Payday lenders charging 400% APR

The same companies that shifted costs are profiting from the debt created by the shifted costs.

The Compound Truth

The costs from Parts 1-9 don’t exist in isolation. They compound:

Emma can’t afford the car (Part 5) because she’s paying:

- Health insurance deductibles (Part 8)

- Credit card interest (Part 4)

- Student loans (Part 1)

- Banking fees (Part 3)

She can’t build savings because she’s paying:

- Monopoly grocery prices (Part 6)

- Monopoly internet prices (Part 7)

- Hundreds in monthly fees (Part 9)

She can’t buy a house because she’s paying:

- Everything above

- Which prevents saving for down payment

- Which forces her to rent

- Which takes 22.8% of income

- Leaving even less for saving

It’s a trap with no exit.

And it’s by design.

What This Means

Emma represents above-median income with no major obstacles (no kids, no chronic illness, no major debt beyond student loans and car).

She can barely survive.

50% of workers make less than Emma.

They’re not surviving. They’re drowning in debt, skipping meals, avoiding healthcare, living paycheck to paycheck with no cushion.

78% of Americans live paycheck to paycheck.

This isn’t because they’re irresponsible. It’s because the math doesn’t work.

The costs have been shifted onto individuals. The wages haven’t increased to cover them. The difference is profit.

What’s Next

We’ve shown you the impossible math (Parts 1-10). Now we’re going to show you exactly where that money went.

Part 11: Who Profits? We’re going to name names. We’re going to show which companies profit from which shifted costs. We’re going to trace the money from your pocket to their bank accounts. And we’re going to show you that it’s the same companies, the same executives, the same shareholders profiting from every single category.

Part 12: The Bipartisan Consensus We’re going to show you how both political parties protect this system. How Democrats and Republicans both take corporate money and both vote to allow these monopolies, these cost shifts, this wealth transfer.

Part 13: How We Got Here We’re going to trace the deliberate policy decisions over 50 years that created this system. The deregulation. The tax cuts. The union busting. The laws that were written by corporate lobbyists and passed by corporate-funded politicians.

Part 14: What We Could Have Instead We’re going to show you other countries where the math actually works. Where healthcare doesn’t bankrupt people. Where education is affordable. Where one job is enough. And we’re going to prove it’s possible because it’s happening right now.

Part 15: How We Get There We’re going to lay out realistic steps to fix this. Not naive optimism. Not simple solutions. Real organizing. Real power-building. Real change. And why it’s worth the decades of work it will take.

Because Emma deserves better than $253/month after working full-time as a nurse.

Because the median worker deserves better than -$572/month.

Because the richest country in world history can do better than forcing 78% of its population to live paycheck to paycheck.

The costs were shifted. Now we shift them back.

Passing the Buck: Why We Pay More But Make Less is a 15-part series examining how corporations and government systematically shifted costs onto working Americans—while wages stagnated and benefits disappeared.

Leave a comment