This is Part 4 of BrokeCon by Design. Part 1: USA! USA! USA! | Part 2: The Words That Stop You From Thinking | Part 3: Follow the Money

Back in Part 3 we ran the receipts: Americans pay around $13,500 per person for healthcare and rank 36th in the world on life expectancy. First in spending, middle of the pack on outcomes.

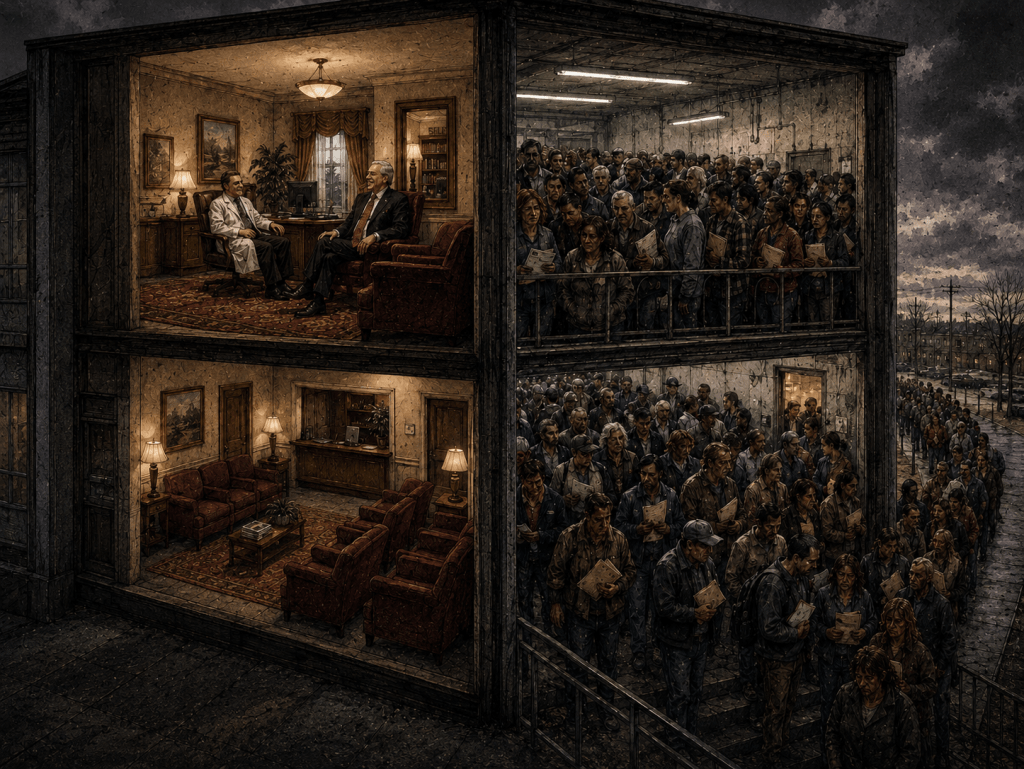

Here’s the part I didn’t get to. The people writing the laws that produced that system don’t actually use it. Not the way you do.

Quick note before we go further: Congress does not have “free lifetime healthcare.” That’s the version your uncle posts on Facebook. The actual setup is mundane and damning — they have an employer-subsidized insurance plan, they happen to work in a building with a Navy doctor on staff, and they walk into Walter Reed when they need to. The gap between that and what they wrote for you is the whole point of this post. If the system they built for the rest of us were genuinely acceptable, they’d use it.

What Congress Actually Has

Since 2014, members of Congress have been required by law to buy their insurance through DC Health Link’s small business exchange. Same general venue as a Washington-area small business owner. So far, so populist.

The federal government, as their employer, kicks in 72% of the premium. That’s a benefit most American small business owners would mug a senator for. The plans are gold tier, covering roughly 80% of expected medical costs. Premium share for a family plan runs around $530 a month out of pocket, with the government covering roughly $1,370 of it. Job-loss risk: roughly zero, since the job is “United States Senator” and the next layoff threat is an election that comes once every two to six years.

On top of the plan, for an annual fee of around $650, members can use the Office of the Attending Physician — a Navy-staffed medical clinic inside the Capitol. Walk in, no appointment. X-rays, lab work, physical therapy, prescriptions. No surgery, dental, or vision (they carry separate coverage for that), but the day-to-day “something hurts and I’d like to know why” part of medicine works the way it should work everywhere: an actual doctor, the same day, no three weeks of phone tag. The going rate for comparable concierge medicine in the private market is $2,000 to $5,000 a year. Congress pays $650.

And they get free outpatient care and discounted inpatient care at Walter Reed and Bethesda. When Mitch McConnell needed a wheelchair after a fall in 2023, one appeared. No prior authorization. No 20% copay. No approved-supplier paperwork. That’s not corruption. That’s just what happens when the system is set up to work.

The detail that should sit with you on that last one: Congress walks into the same military hospital system that veterans wait an average of 20 to 30 days to access. The VA has been underfunded, understaffed, and serially scandaled over waitlists for two decades — long enough that “VA waitlist” is its own news beat. Veterans get the waitlists. Congress gets the same hospitals on demand. Both groups serve the country. Only one of them gets to walk in.

What You Actually Have

You probably have one of three things.

If you’re 65+, you have Medicare. The Part B premium is $185 a month, or $2,220 a year. The deductible is $257. After that, you pay 20% of every covered service for the rest of your life, with no annual cap on out-of-pocket costs. None. Get cancer, get a $40,000 bill. And that’s only Part B. Part A — the hospital side — runs a $1,676 deductible per benefit period; days 61 through 90 of a hospital stay cost you $419 a day in copays; past day 90, it’s $838 a day. Prescriptions aren’t included at all — that’s Medicare Part D, another $40 to $50 a month, plus deductibles, plus the “donut hole” coverage gap where prices spike mid-year. Dental, vision, hearing aids: not covered. Total realistic annual cost for basic Medicare with no catastrophe: $4,500 to $6,500. With a catastrophe, the ceiling is whatever your savings can absorb.

If you’re poor enough, you have Medicaid. The coverage itself is fine — low or no premiums, small copays, comprehensive care. The catch is qualifying. In Texas, a parent of two qualifies for Medicaid only if their household income is below 18% of the federal poverty level. That’s about $4,800 a year. Work 20 hours a week at minimum wage and you make too much. You are literally too poor to afford insurance and too rich to qualify for help. Ten states still refuse to expand the program at all.

If you’re working-age and somewhere in the middle — too well-off for Medicaid, too young for Medicare, no employer plan — you buy on the individual market. Make $60,000 a year? You’re past the subsidy cliff in most states, now that the IRA’s enhanced premium tax credits have expired. A silver plan runs $600 to $750 a month. Annual premium: $7,200 to $9,000. Deductible: $5,000 to $8,000. Out-of-pocket max: $9,200. Network: restricted, regional, and good luck if you get sick on vacation.

Lose your job, lose your coverage. COBRA exists, technically. It costs 102% of the full premium, which is hard to swing when the reason you need it is that you just lost your income.

The Gap, On One Page

| Member of Congress | Median employer plan | Medicare (basic) | Individual market | |

|---|---|---|---|---|

| Employer share of premium | ~72% | ~70% | n/a | 0% |

| Annual premium (family, member share) | ~$6,360 | ~$6,300 | ~$2,200 (Part B, individual) | $7,200–$9,000 |

| Deductible (family) | $1,000–$2,000 | $3,722 | $257 Part B / $1,676 Part A | $5,000–$8,000 |

| Out-of-pocket maximum | $18,400 | $8,764 | None | $9,200 (individual) |

| Walk-in clinic access | OAP, ~$650/yr | No | No | No |

| Military hospital access | Free outpatient at Walter Reed/Bethesda | No | No (even for vets — 20–30 day VA waits) | No |

| Lose coverage if you leave the job | Only if you leave Congress (2–6 yrs guaranteed) | Immediately | Age-based, no | n/a |

| Can rewrite the rules | Yes, literally | No | No | No |

The premium share looks similar between Congress and the median employer plan, which is the part that tends to get left out of the viral version. The differences are everywhere else: smaller deductibles, walk-in access to a Navy doctor for $650 a year, free care at two of the best hospitals in the country, and no chance of being uninsured between now and the next election. The median worker has none of those things and is one bad performance review away from also losing the plan.

The Tell

People float a thought experiment at this point: put Congress on Medicare and Medicaid with no supplemental coverage allowed and watch how fast the system gets fixed. It’s a bumper-sticker fantasy, but the underlying logic isn’t wrong. You can list, fairly cleanly, what would change.

The unlimited 20% Part B coinsurance — perfectly tolerable as policy abstraction, panic attack as personal reality — would get a hard annual out-of-pocket cap within a session. The Part D donut hole would be gone. The provider-acceptance gap that makes Medicaid coverage theoretical instead of actual would close, because the people doing the closing would now be the people being declined. The ten states still refusing to expand Medicaid would expand it the second a senator from one of them tried to use it. Dental, vision, and hearing would get added to basic Medicare. The prior-authorization gauntlet — the thing that lets an insurance company override your doctor — would die the first Friday afternoon a senator’s MRI got kicked back for “medical necessity review.” Drug price negotiation would blow past its current ten-drug pilot fast, because paying $300 for a vial of insulin on a fixed income concentrates the mind.

None of this is hypothetical, by the way. Every other developed country has already done the experiment.

| Country | Spending per person | Life expectancy | Maternal mortality (per 100k) |

|---|---|---|---|

| United States | ~$13,500 | 78.4 | 18.6 (2023); 22.3 (2022) |

| France | $5,700 | 82.5 | ~8 |

| Canada | $5,738 | 82.2 | ~8 |

| United Kingdom | $5,387 | 81.0 | ~7 |

The maternal mortality column is the cleanest single contrast. The US kills mothers in childbirth at roughly two to three times the rate of every country in that table. Same continent of medical knowledge, same century. The difference is the system, not the science. We’re not paying more for the same thing. We’re paying more than twice as much for worse outcomes. The premium is for the privilege of paperwork.

The Receipt

I don’t begrudge Congress having good healthcare. I begrudge them having it while running a separate, demonstrably worse system for the rest of us.

The Office of the Attending Physician exists because waiting three weeks for a rushed 15-minute appointment is bad medicine. The 72% premium subsidy exists because paying full freight is a hardship. The Walter Reed access exists because outpatient care that actually works is a real benefit, not a luxury. They built every one of those workarounds for themselves because they know the alternative — the one they’re handing the rest of us — is the alternative.

About two-thirds of personal bankruptcies in this country cite a medical cause. The healthcare industry spent $743.9 million lobbying the federal government in 2024 — more than any other sector. Pharmaceutical and health-products companies alone accounted for $384.5 million of that. PhRMA, the American Hospital Association, the AMA, and Blue Cross/Blue Shield all sit in the federal top-ten lobbying spenders. Those numbers don’t move in opposite directions to medical bankruptcy by accident.

If the system they wrote for you were acceptable, they’d use it. They don’t.

Next up in Part 5: the genuinely weird American tradition of tying your health insurance to your job — how that happened, why it persists, and what it actually does to the rest of your life.

Sources

Congressional Research Service Report R43194, “Health Benefits for Members of Congress and Designated Congressional Staff.” Office of the Attending Physician reporting: ABC News investigation (2009), American Prospect (2025), GAO Report GGD-75-54. Medicare cost figures: Medicare.gov and CMS, 2025 rates. Medicaid coverage: HHS.gov and state agency data. International spending and life expectancy: OECD Health Statistics. US national health expenditure: CMS National Health Expenditure Data, 2023. Maternal mortality: CDC NCHS (2023 provisional and 2022 final), WHO comparable-country data. VA wait times: GAO reports, VA Office of Inspector General audits. Medical bankruptcy: Himmelstein, Lawless, Thorne, Foohey, Woolhandler, American Journal of Public Health, 2019. Healthcare lobbying expenditures: OpenSecrets federal lobbying database, 2024 totals.

Leave a comment