On October 22, 1986, Ronald Reagan stood on the South Lawn of the White House and signed a tax bill that did something the United States had not done before and has not done since. The Tax Reform Act of 1986 took the top rate on money you make by owning things — long-term capital gains — and set it equal to the top rate on money you make by working. Both capped at twenty-eight percent: the same ceiling for the investor and the electrician, for the first time in modern memory. Reagan called it “a sweeping victory for fairness.” He was not being ironic, and for once the line was close to true.

It was not a left-wing bill. It started as a Democratic proposal from Bill Bradley and Dick Gephardt, got rewritten by a Republican administration, passed a House run by Tip O’Neill and a Senate run by Republicans, and collected large majorities of both parties on the way through. The deal was simple enough to explain at a kitchen table: kill the dozens of shelters and the separate, lower rate for capital, drop the top rate on everyone, and stop pretending the tax code had a reason to care whether a dollar came from a paycheck or a portfolio. For a few years, it actually held. From the law’s first tax year in 1987 through 1990, the top rate on owning and the top rate on working shared the same twenty-eight-percent ceiling.

Then it was taken apart. Not repealed — nobody stood on a lawn and announced the rollback. It came back in pieces. In 1990 a Republican president signed a budget deal that raised the top rate on wages and left the cap on capital where it was, and the gap reopened on its own. In 1993 a Democratic president raised the wage rate again and again left capital alone, and the gap got wider. In 1997 the same administration cut the capital rate outright to twenty percent. In 2003 a Republican one cut it to fifteen and handed the same discount to dividends. In 2013 it settled at the structure we have now, a top rate on capital well below the top rate on work, made permanent by a Democratic administration. Five moves, both parties, twenty-seven years, no single vote you could point to and say that was the one that did it.

That is the whole post in one anecdote. The thing we are told is a law of economic nature — that money from owning simply has to be taxed more gently than money from working, that it would be naive or ruinous to do otherwise — was, recently, not a law of nature at all. It was a setting. A bipartisan Congress flipped the setting off, the sky did not fall, and then the setting got flipped back on so quietly that most people never knew it had been touched.

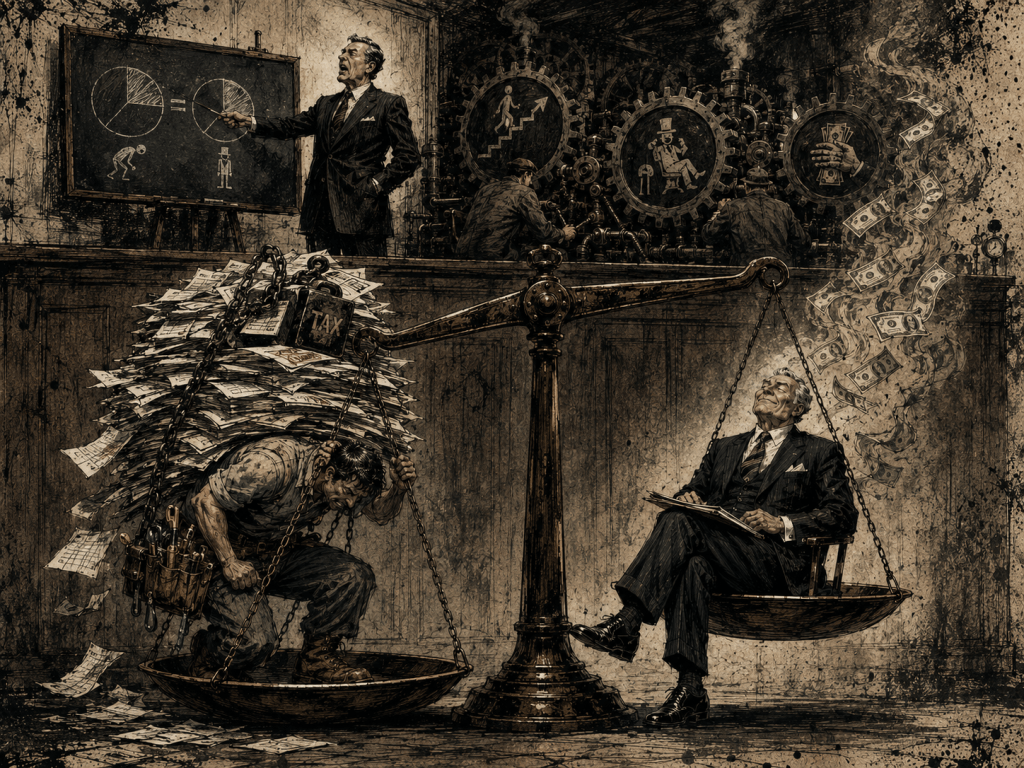

And here is the part this post is actually about. While that re-rigging happened, almost none of the public argument was about it. The argument was about billionaires’ headline rates, about whether the top bracket should be thirty-seven or thirty-nine, about one investor paying less than his secretary. Those fights are real and they are loud and they mostly are not where the money is. The money is in a short list of provisions nobody is fighting about, because they are boring, technical, and enormous, and because the people they enrich have spent a very long time making sure the fight you have instead is the other one.

This is the same argument as the last seventeen posts. The part you were arguing about was never the part that mattered.

The Loud Fight Is Not Where The Money Moves

Start with the size of the thing nobody talks about. Every year the Joint Committee on Taxation publishes a list of what the tax code’s special breaks cost — not spending, but revenue the government chooses not to collect because a provision lets certain income go untaxed or lightly taxed. The total for 2025 was about $2.2 trillion, more than the country spent that year on Social Security, or Medicare, or the military. In dollar terms it is the single largest thing the federal government does. And the biggest items on it are not the ones in the news. The largest individual break in the entire code is the exclusion for retirement accounts — the 401(k) and its relatives, the provision the last post handed straight to this one, worth the most to the highest earners and almost nothing to the workers it is sold as protecting. The second largest is the lower rate on capital gains and dividends. The third is the exclusion for employer health insurance. None of the three is ever a cable segment. Together they move more money than the entire visible argument about tax fairness combines to touch.

So the spine of this post is a contrast, and it runs through everything below. There is a tax debate you are shown — the billionaire whose true rate was a fraction of a percent, the top marginal bracket, the one rich man and his secretary — and there is a tax code that actually exists. The first is mostly a symptom of the second. Arguing the symptom, loudly, for decades, while the provisions underneath it sit untouched, is not a failure of the system. It is one of the ways the system keeps the provisions.

A couple of honest qualifications before the mechanisms, because the argument doesn’t survive without them and this series doesn’t build a strawman just to knock it down. This is not the claim that every break in the code is a scam, or that money from owning has to be taxed exactly like money from working in every case. There are real reasons it is hard. A gain isn’t taxed until you sell it, and that rule exists for a reason — a paper gain isn’t cash, and making someone sell the building or the business to pay a tax bill on money they haven’t actually pocketed is a real problem, not a made-up one. Part of a long-held gain is just inflation, and taxing inflation as if it were real income charges you for a profit you didn’t really get, in a way a paycheck never is. And tax selling hard enough and people stop selling — the money just sits there. None of that is nothing. The honest answer isn’t that the hard parts are fake. It’s that they’re solvable, that other rich countries have solved versions of them, and that the country itself put all three of those arguments on the table in 1986 and a Congress of both parties decided they did not outweigh taxing the two kinds of income the same. That is the difference between a hard problem and an excuse. This post is about how the breaks are handed out and how quietly large they are, not a claim that the questions underneath them aren’t real questions.

And mostly, this is a consensus, and the post isn’t going to pretend otherwise in either direction. The lower rate on money from owning got reopened under one president, widened under the next, and cut again under the one after that. Step-up in basis is bipartisan. Carried interest has outlasted presidents of both parties who promised, by name, to kill it. There is no clean villain to point at for those, and inventing one would be its own dishonesty. But two pieces are not symmetric, and pretending they are would be the opposite dishonesty. The 2017 tax law and the 2025 law that made it permanent were one-party bills, moved through reconciliation on near-party-line votes — the 2025 one locked the estate-tax exemption in at fifteen million dollars a person and cleared the House two hundred eighteen to two hundred fourteen without a vote from the other side. And the long, deliberate work of starving the tax collector so the code we already have never gets enforced on the people best able to dodge it — plus the rebranding of the estate tax as the “death tax” — has come overwhelmingly from one direction. The consensus is real. So is the asymmetry. Saying both, and letting neither excuse the other, is the whole job here.

One of those two asymmetric pieces belongs here, because it sits underneath everything that follows. A provision only matters if it is enforced, and the part of the code aimed at the high end increasingly is not. The 2022 Inflation Reduction Act gave the IRS about $79 billion over a decade, which the Congressional Budget Office estimated would bring in roughly $204 billion by collecting taxes already legally owed. Then it was clawed back — a piece in the 2023 debt deal, more in 2024 and 2025, roughly twelve billion more at the start of this year — until about two-thirds was gone. On top of that the agency lost around a quarter of its staff in 2025, including roughly a third of the revenue agents, the people who do the slow, complex audits of wealthy individuals and partnerships. You cannot evade a wage; it is reported and withheld before you see it. You can evade a great deal else, and the part of the IRS that catches it is the part that was deliberately taken apart. Keep that underneath the rest. The provisions below are how the code is written. The enforcement collapse is how the code, as written, stops applying to the people it is written around.

Four Ways The Money Gets Out, In Order Of How Completely

The cleanest way to see the code is to follow a dollar of gain and watch how far it can get from the tax collector, starting with the provision where it is at least taxed something and ending with the one where it is never taxed at all. Four steps. None is an accident, each has a beneficiary you can name, and each one sits right next to a louder fight that keeps your attention off it.

The first step is the rate gap, the floor everything else is built on. Money you make by working is taxed up to thirty-seven percent, plus payroll tax on top. Money you make by owning — long-term capital gains, qualified dividends — tops out at twenty percent, twenty-three point eight with the investment surtax, and no payroll tax at all. That is not a market outcome or an economic constant. It is a number Congress writes down, and the proof it is a choice is the 1986 story at the top of this post: for several years it was written down as the same ceiling for both, and the country kept functioning. Who gets the lower number is not a mystery. In 2023, households making over a million dollars reported, on average, around eight hundred thousand dollars of capital gains apiece — about a quarter of their entire income arriving at the discounted rate. Households under a hundred thousand reported, on average, around three hundred dollars. The loud fight next door is the one about the top marginal bracket, thirty-seven versus thirty-nine — a real fight about a rate most of this money never pays, because it is not labor income and the whole point of the structure is that it isn’t.

The second step is the one nobody even calls a subsidy, which is why it works. The code is full of deductions and exclusions whose dollar value rises with your bracket, so the same benefit is worth more the richer you are. This is the retirement exclusion the last post ended on: a dollar you don’t pay tax on is worth thirty-seven cents to someone in the top bracket and ten cents to someone in the bottom one, so the “help people save” provision delivers the most help to the people who need it least and were going to save anyway. The same upside-down shape runs through the employer-health exclusion, the mortgage-interest deduction, and the twenty-percent pass-through deduction the 2017 law created and the 2025 law made permanent. The Joint Committee on Taxation found that eighty-four percent of the benefit from the state-and-local, charitable, and mortgage deductions in 2025 went to households making over two hundred thousand dollars. There is a long, loud politics of “welfare” in this country aimed at programs for the poor. The largest welfare in the code goes up the income scale through provisions that are never called welfare, because they arrive as a smaller tax bill instead of a check, and a smaller tax bill doesn’t feel like a benefit even when it is the biggest one in the budget.

The third step is the cleanest example in the entire code of a rule written for one specific group, and it is worth dwelling on precisely because it is small. Carried interest is the share of investment profits private-equity and hedge-fund managers take as their pay — the “twenty” in “two and twenty.” It is compensation for managing other people’s money. By any plain reading it is labor income, and a teacher’s labor income is taxed as labor income. A fund manager’s is taxed as a capital gain, at the lower rate, because the code was written to let it be. What makes this the cleanest case is not its size; the Joint Committee on Taxation’s score for closing it runs on the order of sixty-some billion dollars over ten years, close to a rounding error against a multi-trillion-dollar code. It is the cleanest case because it is that small and still here. It is one statutory paragraph. Presidents of both parties have promised, by name, to end it, for nearly twenty years. The 2025 law rewrote the tax code top to bottom, on one party’s votes, could have closed it with a sentence, and chose not to. A provision that cheap, that indefensible on the merits, promised dead that many times and still breathing, is not a loophole that survived by accident. It is the consensus, holding still long enough to be photographed.

The fourth step is the one where the money is not taxed less or taxed late but never taxed at all, and it is three provisions working as one machine. Start with the realization rule: a gain is not income until you sell, so an asset that rises in value for forty years is, for those forty years, untaxed. The very wealthy do not sell. They borrow against the appreciated asset instead — a loan is not income, so the cash to live on arrives tax-free — and they hold the asset until death. At death, step-up in basis resets the asset’s cost to its value on the day the owner dies. The entire lifetime gain, the forty years of appreciation never taxed because it was never sold, is not deferred to the heirs. It is erased. The heir who sells the next day owes nothing. The Joint Committee on Taxation puts the cost of the step-up alone in the neighborhood of seventy billion dollars a year, on the order of a quarter of everything the capital-gains tax brings in. And the estate tax, the one backstop that used to catch the transfer itself, has been hollowed out: the exemption climbed from six hundred thousand dollars a generation ago to roughly fourteen million per person, and the 2025 law made it permanent at fifteen million, indexed to rise forever, on a party-line vote. The loud fight here is the “death tax,” a phrase engineered for a tax that now reaches a fraction of the top one percent of estates. The quiet fact is the machine the phrase guards: buy, borrow, die, and a fortune’s worth of gain passes through an entire human life and out the other side having never once been income.

That last step has a live legal edge worth stating precisely, because both sides overstate it. In 2024 the Supreme Court decided Moore v. United States, routinely described as having settled whether the government can tax wealth or unrealized gains. It did not. The Court upheld a narrow 2017 provision — a one-time tax on the accumulated, undistributed earnings of certain foreign companies — on the ground that the income had been realized at the company level and Congress has long been allowed to attribute a company’s income to its owners. The majority went out of its way to say in a footnote that it was not deciding whether the Constitution requires income to be “realized,” and not addressing taxes on wealth, net worth, or appreciation. So the question is open. But four justices signaled they think realization is constitutionally required, and one said flatly it is not, which means the hardest version of the fix at the bottom of this post — taxing the gains the rich never realize — is not just a political fight but an unsettled constitutional one. Saying it is already won, or already lost, is the same overstatement, and the post is not going to make it.

What’s Real

A few honest qualifications, because the strongest version of the argument is the one that doesn’t pretend the counter-arguments aren’t there.

The realization rule is not a trick someone slipped into the code. Taxing a gain you have not turned into cash is a genuine administrative problem, and the version that hits hardest is not the billionaire. It is the person who owns one illiquid thing — a farm, a family business, a building — that has gone up on paper, who would have to sell part of the thing itself to pay tax on money they have not received. That objection is real, and any fix that ignores it deserves to lose. The inflation point is real too: hold an asset thirty years and a chunk of the “gain” is just the dollar being worth less, and taxing that part at full rates overstates the profit in a way a wage is never overstated. The lock-in effect is real and measurable: tax selling hard enough and people don’t sell, and capital freezes in place. And there is a coherent argument that corporate profits are taxed once at the company and again at the shareholder, so the lower second rate is partly correcting a double count.

None of those is nothing, and the point of this post is not that they are. The point is what the country did with them in 1986: it put all of them on the table — administrability, inflation, lock-in — and a bipartisan Congress decided they were real but solvable, and not a good enough reason to keep taxing the janitor’s income harder than the shareholder’s. The hard parts are hard. They have been solved, in pieces, here and elsewhere: inflation indexing, thresholds that exempt the genuinely illiquid estate, deferral with interest for the family business. The argument is not that the problems are imaginary. It is that they are the reason given for a structure whose actual job is the distribution in the section above, and that “this is hard” has been doing the work of “this cannot be done” for forty years, by people who know the difference.

What They’re Paying For

What the rigged code actually produces, set against what the tax debate claims to be about, is four things stacked together. Each is worth real money to someone specific, and the someone is nameable in every case, which is the difference between this and a complaint about “the rich.”

It is a permanent discount on a kind of income one group overwhelmingly has and another structurally does not. The household with eight hundred thousand dollars of annual gains and the household with three hundred are not paying different rates because one worked harder. They are paying different rates because one’s income is the kind the code was built to favor. The beneficiary is the asset-owning top of the distribution, specifically, and the discount is the single largest reason the billionaire-versus-secretary anecdote is true — not as a scandal, but as the system working exactly as written.

It is a wall of subsidies aimed over the heads of the people they are sold to protect. The retirement break, the health break, the housing break, the pass-through break: every one is justified by an ordinary person — the saver, the homeowner, the small business — and every one delivers most of its value to the top because its value rises with the bracket. The beneficiary is the high earner who would have saved, owned, and incorporated anyway, collecting the largest version of a benefit named after someone else.

It is an entire profession’s pay reclassified into the favored category, and a planning industry that exists to do the same trick for everyone else. The carried-interest paragraph is the clean case; the GRATs and dynasty trusts and valuation discounts around the hollowed estate tax are the same logic sold as a service. The beneficiary is the fund managers whose labor is taxed as capital, and the lawyers and advisers whose business is moving other people’s income across that same line, profession by profession, estate by estate.

And it is a structure that, at the very top, removes the income from the tax base entirely and then defends the removal with a fight about something else. Buy, borrow, die is not deferral. It is disappearance. The beneficiary is the dynastic holder whose gain is never realized, never borrowed into a taxable event, and erased at death — and the political actors who took the donations, protected the provisions, defunded the one agency that could have checked any of it, and renamed the estate tax so the public would guard the gate for them. That is the bill the loud argument has been keeping you from reading.

The Fixes Are Boring

The fixes below are structural, not slogans. The post is not going to put “simplify the code” or “flatten the brackets” or “abolish the IRS for everyone under ten million” on the list, because those are not solutions to a designed transfer — the last one is the transfer wearing a populist hat, since gutting the agency is precisely how the code stops applying at the top. These sound impossible because the people who profit have spent decades making them sound impossible and making the headline fight the one you have instead, not because they are radical or untested. Several are what the United States itself did, recently, before it chose not to. Roughly cheapest and most immediate to genuinely hard:

- Close carried interest in a single paragraph. Treat the fund manager’s profit share as what it is, compensation for labor, taxed like everyone else’s labor. No phase-in, no carve-out. It has been “about to be closed” under presidents of both parties for almost twenty years, and a one-party bill that rewrote the whole code in 2025 still left it standing, which tells you the obstacle was never drafting difficulty.

- Ring-fence durable IRS enforcement funding aimed at the high end, and stop letting it be clawed back. This is an appropriation, not a new institution. The 2022 funding was projected to return roughly two and a half dollars for every dollar spent, and about two-thirds of it has since been rescinded while a quarter of the staff, including a third of the complex-audit agents, was lost. The diluted version — fund it, then let each subsequent budget quietly take it back — has already been tried, on purpose. Make the high-end enforcement money multi-year and protected from the annual rescission.

- Tax income from owning at the same rate as income from working. Say it plainly: this is not a novelty, it is a return to the 1986 settlement that a bipartisan Congress already enacted and the country already lived through without collapse. Every diluted version since — a small bump, a high threshold, a sunset — was built to be reversible and was reversed. Equalize the top rates and pair it with the basis fix below so it cannot simply be routed around by never selling.

- End step-up in basis and treat death, gift, or a large borrow against appreciated assets as a realization event above a real threshold. The lifetime gain should be taxed once, somewhere, before it is erased. Exempt the genuinely illiquid estate with a threshold and a deferral-with-interest option for the family farm or business — the real version of the carve-out the watered-down bills used as a poison pill rather than a fix. The point is the buy-borrow-die exit, and the fix is to make at least one of those three steps a taxable moment.

- Convert the upside-down deductions and exclusions into flat refundable credits. This is the structural answer to the provision the last post handed over. A deduction is worth more the higher your bracket; a flat credit is worth the same to everyone, and a refundable one reaches the people with no tax liability to deduct against at all. Do it to the retirement, mortgage, and health exclusions and the subsidy stops being aimed over the heads of the people it is named for. The smaller versions failed because they were designed to preserve the tilt while looking like reform.

- Restore the estate tax to a real exemption and a real rate, and close the trust machinery around it. The GRATs, the dynasty trusts, the valuation discounts were specific instruments built by a specific industry to make the nominal rate optional for the people nominally subject to it. Lower the exemption, mean the rate, and shut the instruments. The 2025 law moved hard in the opposite direction, permanently, on one party’s votes; naming that is not partisanship, it is the date and the vote count.

- Tax the gains the very top never realizes — and do it knowing this is the genuinely hard one. Some form of mark-to-market or minimum tax on the largest unrealized fortunes is the only thing that actually reaches buy-borrow-die at the level where it operates. It is last because it is hardest: it carries the real administrability problems from the section above, it needs the inflation and illiquidity answers built in rather than waved away, and after Moore it carries a live constitutional question that is genuinely unresolved. The honest position is not that this is easy. It is that the difficulty is a reason to design it carefully, not a reason to keep pretending the other six items are radical so this one never gets discussed at all.

Six of the seven are a statute or an appropriation — things a Congress or an administration could do without inventing anything. The seventh is the one the country has not tried and the courts have not settled, and it is honest to say so rather than pretend the list is all easy. None of them is the radical position. The radical position, by the standard of 1986, is the one we are living in, where the country looked at taxing the two kinds of income the same, did it, watched nothing break, and then spent twenty-seven years quietly undoing it while the public argued about the rate on the bracket most of the money never touches.

Who Is This For

The retirement system moved the risk onto you and called it freedom. The tax code does the same work one layer up, and it does not even need the story about freedom to do it — it just needs the argument to stay on the rates in the headlines while the money moves through the provisions in the footnotes. What you were shown is not where the money is. The next post takes this exact machine and moves it from the person to the company: the same logic that lets the owner’s gain go untaxed lets the corporation’s profit go untaxed, and Part 19 is how some of the largest companies in the country post record profits and pay zero federal income tax, legally, in the same years. Different layer. Same question.

Leave a comment