Paying More While Farmers Make Less

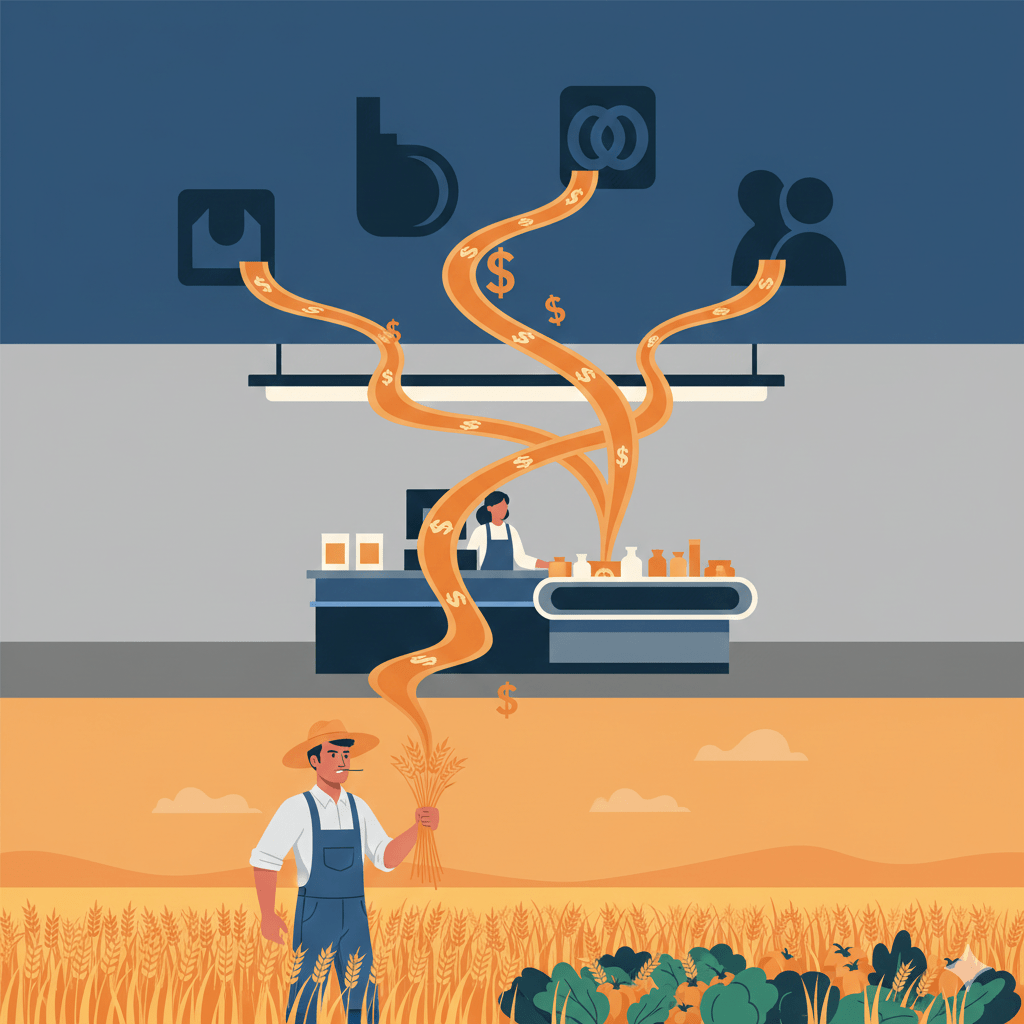

Let’s follow a gallon of milk from farm to your refrigerator.

At the dairy farm in Wisconsin: Tom has been dairy farming for 30 years. He has 150 cows. He wakes up at 4:30 AM every day—no weekends, no holidays. Cows need milking twice a day, every day.

His cows produce about 9,600 gallons of milk per day. He sells it to the regional processor for $0.38 per gallon.

Daily revenue from milk: $3,648

Sounds decent, right? But Tom’s daily costs:

- Feed: $1,200

- Labor (him + 2 employees): $650

- Veterinary care and medicine: $280

- Equipment maintenance: $350

- Electricity and water: $180

- Mortgage on land and equipment: $520

- Insurance: $120

- Fuel: $85

Daily costs: $3,385

Daily profit: $263 (if nothing breaks, no cows get sick, no unexpected costs)

Tom works 365 days a year, 14+ hours a day, and nets $95,995 annually if everything goes perfectly. Which it doesn’t.

Last year, one of his milking machines broke ($6,800), three cows got sick and died ($9,000 loss), and feed prices spiked 18% mid-year.

Tom’s actual take-home: $68,000 for the year. For 5,110 hours of work. That’s $13.30/hour.

At the processing plant: The processor (likely Dean Foods or one of the three other companies that control 80% of milk processing) buys Tom’s milk for $0.38/gallon. They pasteurize it, bottle it, and sell it to grocery distributors for $2.85/gallon.

Processor margin: $2.47 per gallon

At the grocery store: Kroger (or Walmart, or Albertsons, or one of the four chains that control 60% of grocery sales in most regions) buys the milk for $2.85/gallon and sells it to you for $4.49/gallon.

Grocery margin: $1.64 per gallon

Total:

- Farmer gets: $0.38 (8.5% of what you pay)

- Processor gets: $2.47 (55%)

- Grocery store gets: $1.64 (36.5%)

Tom works 14-hour days, 365 days a year, manages 150 living animals, deals with all the risk, and gets 8.5 cents per dollar you spend on milk.

The processor and grocery store get 91.5 cents per dollar for moving and selling what Tom produced.

And here’s the kicker: Tom can’t negotiate. There are only four milk processors in his region. They all pay the same price. If Tom doesn’t like it, he can go out of business.

Which is exactly what’s happening.

The Consolidation of Food

In 1970, Tom’s father sold milk to one of 15 competing processors in the region. Today, there are four. When Tom started farming in 1994, there were still seven.

This isn’t just milk. This is everything you eat.

Meat Processing: Near-Total Control

Beef:

- Tyson Foods: 24% market share

- JBS USA: 23%

- Cargill: 22%

- National Beef: 14%

Combined: 83% of all beef processing in America

Pork:

- Smithfield Foods (owned by China’s WH Group): 26%

- Tyson Foods: 18%

- JBS USA: 16%

- Hormel: 11%

Combined: 71% of all pork processing

Chicken:

- Tyson Foods: 20%

- Pilgrim’s Pride: 18%

- Sanderson Farms: 12%

- Perdue Farms: 10%

Combined: 60% of all chicken processing

Four companies control what America eats for protein. If you eat meat, you’re buying from one of four companies no matter which brand you choose.

Grocery Retail: Your Illusion of Choice

Walk into a Kroger. Walk into a Ralphs. Walk into a Fred Meyer, Fry’s, Smith’s, King Soopers, QFC, or City Market.

Same company. Kroger owns all of them.

Walk into Safeway, Albertsons, Vons, Pavilions, Randalls, Tom Thumb, Shaw’s, Star Market, Jewel-Osco, or Acme.

Same company. Albertsons owns all of them.

Top grocery retailers (2024):

- Walmart: 25% market share

- Kroger: 10%

- Costco: 7%

- Albertsons: 5%

Top 4 control: 47% of grocery sales

And Kroger is trying to buy Albertsons for $24.6 billion. If approved, one company would control 15% of the U.S. grocery market, with over 5,000 stores.

That would give them pricing power in most American cities. If you don’t like Kroger’s prices, where else will you shop?

The Seeds, the Feed, the Fertilizer: Also Monopolized

It’s not just processing and retail. The inputs farmers need are also controlled by a handful of companies.

Seeds:

- Bayer (Monsanto): 26% market share

- Corteva (DuPont Pioneer): 21%

- ChemChina (Syngenta): 8%

Top 3 control: 55% of commercial seed market

Fertilizer:

- Nutrien: 23% of North American market

- CF Industries: 19%

- Mosaic: 15%

Top 3 control: 57% of fertilizer

Farm Equipment:

- John Deere: 53% of large tractors

- CNH Industrial (Case IH): 19%

Farmers like Tom are squeezed from both sides:

- Pay monopoly prices for seeds, fertilizer, equipment

- Sell to monopoly processors at take-it-or-leave-it prices

They have no pricing power. None.

The Price Surge: Inflation or Gouging?

Remember the “inflation” of 2021-2023? When your grocery bill skyrocketed and politicians blamed COVID supply chains?

Let’s look at what actually happened.

Grocery Prices (2020-2024):

- Overall food prices: Up 25%

- Eggs: Up 60%

- Beef: Up 38%

- Chicken: Up 28%

- Milk: Up 18%

- Bread: Up 22%

What about costs?

Input Costs (what farmers pay):

- Feed corn: Up 12% (peak was up 40%, then fell)

- Diesel fuel: Up 15% (peak was up 80%, then fell)

- Fertilizer: Up 8% (peak was up 60%, then fell)

Costs spiked briefly in 2021-2022, then fell back. Prices stayed high.

Corporate Profits (2020-2023):

Tyson Foods:

- 2020 net income: $2.1 billion

- 2023 net income: $2.6 billion

- Increase: 24%

Kroger:

- 2020 net income: $1.9 billion

- 2023 net income: $2.2 billion

- Increase: 16%

Walmart:

- 2020 net income: $13.5 billion

- 2023 net income: $15.3 billion

- Increase: 13%

General Mills:

- 2020 net income: $2.2 billion

- 2023 net income: $3.1 billion

- Increase: 41%

Archer Daniels Midland (grain processor):

- 2020 net income: $1.8 billion

- 2023 net income: $3.6 billion

- Increase: 100%

Costs went up briefly, then came down. Prices stayed high. Profits soared.

This wasn’t inflation. This was price-gouging enabled by monopoly power.

When four companies control 83% of beef processing, they don’t compete on price. They coordinate. Not in a smoke-filled room—they don’t need to. They just follow each other’s price increases.

Tyson raises prices 10%. JBS sees they can do the same. Cargill follows. National Beef follows. Consumers have no alternative—buy beef at the new price or don’t buy beef.

Repeat for every category.

Shrinkflation: You’re Paying More for Less

Can’t raise prices too obviously? Just give people less.

Examples (2020-2024):

- Gatorade: 32oz bottle → 28oz bottle (same price)

- Charmin: 244 sheets per roll → 220 sheets (same price)

- Bounty: 165 sheets per roll → 147 sheets (same price)

- Doritos: 9.75oz bag → 9.25oz bag (same price)

- Tillamook ice cream: 56oz → 48oz (same price, 14% less product)

- Folgers coffee: 51oz → 43.5oz (same price)

- Crest toothpaste: 4.1oz → 3.8oz (same price)

You’re not imagining it. The package looks the same size. The price is the same or higher. But there’s less product inside.

This isn’t cost-driven. This is profit-driven.

And who’s doing it? The same handful of companies that control each category:

- Procter & Gamble (Charmin, Bounty, Crest): 60% market share in their categories

- PepsiCo (Gatorade, Frito-Lay/Doritos): 24% of U.S. beverage market

- J.M. Smucker (Folgers): 35% of U.S. coffee market

- Tillamook: Actually a cooperative (smaller company, still had to compete with price increases)

When you control the market, you can shrink products without losing customers. Where else will they go?

What Farmers Get: The Shrinking Share

Remember, Tom the dairy farmer gets $0.38 per gallon when you pay $4.49. That’s 8.5%.

That’s actually worse than historical averages.

Farmer share of food dollar:

- 1970: Farmers got 32 cents of every food dollar

- 1980: 31 cents

- 1990: 25 cents

- 2000: 19 cents

- 2010: 16 cents

- 2020: 14.3 cents

2024: 14.3 cents per food dollar (latest data)

Farmers’ share has been cut in half since 1970. Meanwhile, food prices have increased faster than inflation.

Where did that money go?

Marketing and processing: 85.7 cents per food dollar

That’s the processors, distributors, and retailers. The middlemen. The monopolies.

The Cattle Example

A rancher raises a steer for 18-24 months. Feed, veterinary care, land, labor. When it’s ready for slaughter at 1,200-1,400 pounds, the rancher sells it to a packer.

What the rancher gets: ~$1,400 (about $1.00-1.20/lb live weight)

The packer processes it into about 600-700 pounds of retail cuts.

What you pay at the store: ~$4,200 (about $6/lb for ground beef, $12-20/lb for steaks, average ~$6/lb)

Breakdown:

- Rancher: $1,400 (33%)

- Packer/processor: $1,800 (43%)

- Retailer: $1,000 (24%)

The rancher spent two years raising that animal. The packer processed it in a few hours. The retailer sold it in a few days.

The rancher got 33%. The middlemen got 67%.

And here’s the thing: In 1980, ranchers got 62% of the retail price of beef. Today: 33%.

The shift happened as processing consolidated from dozens of regional packers to four national corporations.

The Farmer Trap: No Alternatives

Tom the dairy farmer can’t just switch buyers. Here’s why:

Geographic monopolies: Milk is heavy and spoils quickly. Tom can only sell to processors within about 100 miles. In his region, there are four processors. They all pay the same price ($0.38/gallon).

If Tom doesn’t like it, he can:

- Sell at their price

- Dump the milk (illegal due to environmental regulations)

- Stop producing (go out of business)

Contract farming: Many farmers don’t even own their animals anymore. In chicken farming, for example:

- Tyson or Pilgrim’s Pride owns the chickens

- Farmer owns the land and houses

- Company dictates feed, medicine, and methods

- Farmer is paid per pound of chicken raised

- Farmer bears all the risk (disease, death, equipment failure)

- Company sets the price

If the farmer doesn’t like the terms, the company stops delivering chicks. The farmer has houses worth $500,000 and no chickens to put in them.

60% of chicken farmers live below the poverty line despite working 70+ hour weeks.

Farm Bankruptcies

This isn’t sustainable:

Farm bankruptcies (Chapter 12):

- 2019: 595 filings

- 2020: 621

- 2021: 519

- 2022: 493

- 2023: 559

Farm debt:

- Total farm debt: $536 billion (2024)

- Average farm debt: $1.3 million

Farmers going out of business:

- 1950: 5.4 million farms in the U.S.

- 1980: 2.4 million

- 2000: 2.2 million

- 2020: 2.0 million

We’re losing farms while food companies post record profits.

And when a farm goes under, who buys the land?

Corporate Land Grab

Bill Gates is now the largest private farmland owner in America:

- Owns 269,000 acres across 18 states

- Total farmland value: ~$1 billion

But Gates is small compared to corporations:

Farmland ownership (2024):

- Institutional investors (pension funds, sovereign wealth funds): 15-20% of U.S. farmland

- Foreign investors: 40 million acres (3% of all U.S. agricultural land)

When farms fail, corporations and investors buy the land. They lease it back to farmers or hire farm managers.

The farmer becomes a laborer on land their family owned for generations.

Who Profits?

Tyson Foods (2023):

- Revenue: $53.0 billion

- Net income: $2.6 billion

- CEO Donnie King compensation: $13.7 million

Tyson processes:

- 20% of all beef in America

- 20% of all chicken

- 18% of all pork

If you eat meat, you probably ate something Tyson processed this week.

Kroger (2023):

- Revenue: $150.0 billion

- Net income: $2.2 billion

- CEO Rodney McMullen compensation: $19.1 million

Kroger operates 2,800 stores under 28 different brand names. You might not know you’re shopping at Kroger, but you probably are.

Walmart (2023):

- Revenue: $611.3 billion

- Net income: $15.3 billion

- CEO Doug McMillon compensation: $26.0 million

Walmart sells 25% of all groceries in America. In many rural areas, they’re the only option.

Cargill (Private company, 2023 estimates):

- Revenue: $177 billion

- Net income: $6-7 billion (estimated)

- Ownership: Cargill family (14 billionaires on Forbes 400)

Cargill controls:

- 22% of beef processing

- 26% of grain trading

- Massive portions of animal feed, fertilizer, and food ingredients

The Cargill family became billionaires by standing between farmers and consumers and extracting value from both.

The Shift: From Competition to Monopoly

1980s Food System:

- Beef processing: Top 4 controlled 36% → Today: 83%

- Pork processing: Top 4 controlled 34% → Today: 71%

- Broilers (chickens): Top 4 controlled 35% → Today: 60%

- Seeds: Hundreds of companies → Today: 3 control 55%

- Grocers: Regional chains, local stores → Today: 4 control 47%

What changed?

Reagan-era deregulation:

- Relaxed antitrust enforcement

- Allowed mergers that created monopolies

- “Efficiency” became the only consideration (not competition, not consumer welfare)

The result:

- 1980: 50 major meat processing companies

- 2024: 4 companies control 70%+ of each meat category

Who lobbied for this?

- Food processing companies

- Grocery chains

- Agricultural input companies

Who paid for it?

- Farmers (lower prices)

- Workers (lower wages, worse conditions)

- Consumers (higher prices)

Who profited?

- CEOs (multimillion-dollar compensation)

- Shareholders (record profits)

- Private equity (buying up farms and food companies)

Sarah, Jason, Jennifer, Maria, and Tom

Let’s check in on our people from previous parts:

Sarah (the nurse from Part 1):

- Monthly food budget: $450

- 2020 cost for same groceries: $360

- Increase: 25%

- Her wage increase: 3%

Jason (the teacher from Part 4):

- Monthly food budget: $520 (family of 3)

- 2020 cost: $416

- Had to put groceries on credit cards during wife’s layoff

- Credit card balance: $11,400

Jennifer (the pharmacy tech from Part 5):

- Monthly food budget: $400

- 2020 cost: $320

- Between car costs and food costs, she’s $220 short every month

Maria (home health aide from Part 3):

- Monthly food budget: $280 (very tight, lots of rice and beans)

- 2020 cost: $224

- Overdraft fees came partially from grocery transactions

Tom (dairy farmer from Part 6):

- Works 365 days/year, 14+ hours/day

- Makes $13.30/hour after all costs

- Gets 8.5 cents per dollar you spend on his milk

- Can’t negotiate because four companies control milk processing

The connection: Tom gets paid less for his milk. Sarah, Jason, Jennifer, and Maria pay more for groceries. The processors and retailers collect the difference.

Tyson, Kroger, Walmart, and Cargill profit from both ends.

The Illusion

They tell you it’s inflation. They tell you it’s supply chain problems. They tell you it’s “market forces.”

It’s none of those things.

It’s monopoly pricing.

When four companies control 83% of beef, they don’t compete. They coordinate. Prices go up together. They stay up together.

When Kroger and Albertsons control most grocery stores in your city, you pay what they charge. You have no alternative.

When three companies control 55% of commercial seeds, farmers pay what they charge. They have no alternative.

This isn’t a free market. This is extraction.

And the same companies fighting antitrust enforcement—spending millions lobbying Congress—are the ones raising your grocery bill while squeezing farmers into poverty.

What’s Next

We’ve covered housing, healthcare, education, banking fees, credit cards, cars, and now food. All showing the same pattern:

- Consolidation into monopolies

- Prices rising faster than costs

- Record corporate profits

- Workers and consumers squeezed

In Part 7, we’re looking at phone and internet service—another “mandatory” expense where you have no real choice, providers don’t compete, and you pay far more than people in other countries for worse service.

Spoiler: It’s the same playbook. Monopoly, extraction, profit.

Because once they figured out the formula, why stop?

Passing the Buck: Why We Pay More But Make Less is a 15-part series examining how corporations and government systematically shifted costs onto working Americans—while wages stagnated and benefits disappeared.

Leave a comment