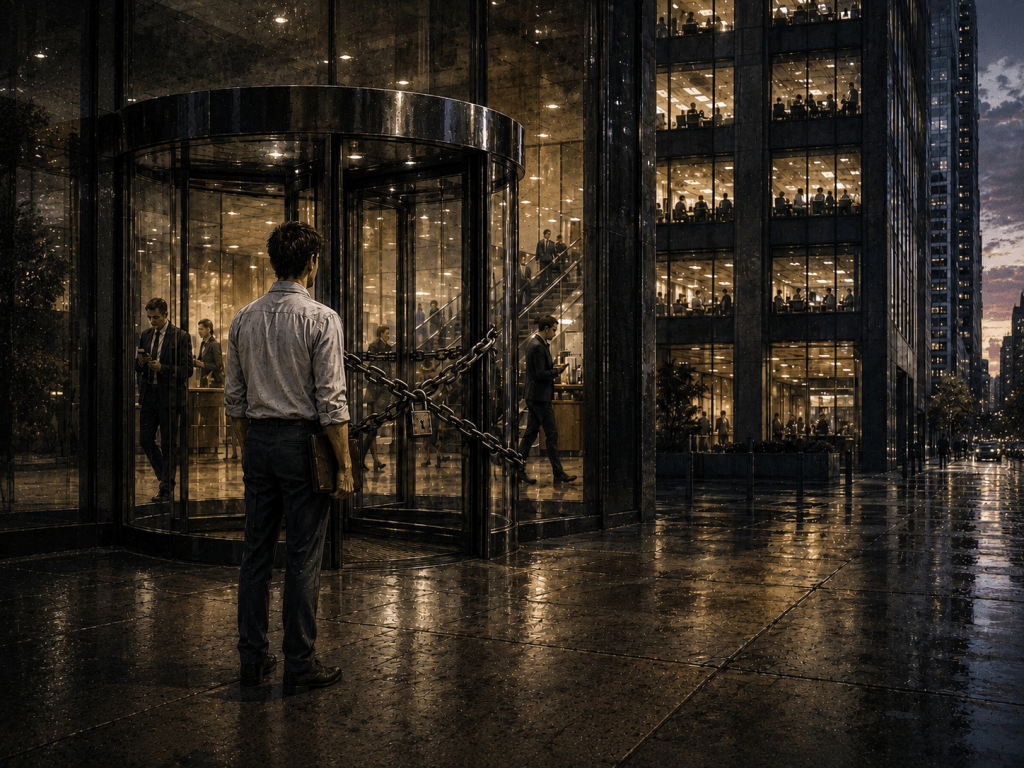

The Door Is Already Locked

Say you’re thirty-two. You have an idea for a business. Maybe a good one, maybe not, but you want to find out. So you sit down and run the numbers.

The first thing that kills it is the healthcare math. Your employer pays most of your premium right now. Walk away and you’re shopping the ACA marketplace, where a comparable plan runs several hundred dollars a month with a deductible that can clear $7,000 before coverage really starts. (The average single-coverage deductible for employer plans in 2025 is $1,886, but the cheaper marketplace plans are noticeably worse — KFF Employer Health Benefits Survey.) If you’re married and your spouse needs coverage too, you’re in family-premium territory — averaging $26,993 a year for employer-sponsored coverage, of which the worker typically pays about $6,850 out of pocket. Off the employer plan, you’re paying the whole thing.

Then the housing math. The median age of a first-time homebuyer is now forty (NAR’s 2025 Profile of Home Buyers and Sellers, a record high — it was around thirty as recently as 2010), so you’re almost certainly still renting. The national median two-bedroom rent runs around $1,895 (Zumper). In a city where customers actually live, you’ll pay $2,500 or $3,500.

Then the student loan payment, which doesn’t pause for entrepreneurship and can’t be discharged in bankruptcy.

You add it up. You don’t start the business. The idea wasn’t bad. The door is already locked.

Three Locks, One Door

This is the post in this series I’ve been trying to figure out how to write since I started writing it. Healthcare made the case in Part 5 (Employer-Based Health Insurance: Modern Serfdom). Housing made the case in Part 7 (The Housing Trap). Student debt and childcare made the case in Part 8 (The Education and Childcare Cliff). Each one of those is its own extraction, and each would be worth a fight on its own merits. But they don’t actually function as three problems. They function as three locks on the same door.

The door is the ability to leave. Leave a job. Leave a city. Leave a marriage you stayed in for the insurance. Leave a career you don’t want anymore. Leave the path you were on at twenty-two when somebody at a college fair told you the loans would be worth it.

Any one lock you can sometimes pick. Pay down the debt and you’ve shaved a few hundred dollars off the monthly nut. Move to a cheaper city and you’ve cut the rent. Find an employer with better insurance and you’ve taken one anxiety off the table. But the locks are connected. Solving for one usually breaks something somewhere else — you take the cheaper apartment in the cheaper city, and now there’s no job there in your field with the benefits you needed in the first place. You change employers for the insurance, and the new job pays less and is two states away from your kid’s school.

That’s not a coincidence. That’s the system working.

How Each Lock Got Built

None of this was inevitable, and three short paragraphs are not going to do justice to any of the histories. But the pattern across them is worth looking at all in one place.

The healthcare lock is a WWII accident nobody bothered to fix. The Stabilization Act of 1942 froze wages but exempted “insurance and pension benefits” from the freeze. A 1943 War Labor Board ruling, backed by the IRS the same year, made employer-paid health insurance tax-free to the worker. In 1954, Congress codified the exclusion in Section 106 of the Internal Revenue Code. The result, eighty-some years later: 154 million Americans get their coverage through their employer, and walking off the job costs them their access to the doctor. Every other developed country eventually untied this knot. We didn’t, because the people who profit from it — the insurers, the large employers who like the leverage — kept paying enough money to the right people to make sure we didn’t.

The housing lock starts in the 1920s. Buchanan v. Warley (1917) struck down explicit racial zoning, so cities pivoted to exclusionary zoning that didn’t say the quiet part out loud. Euclid v. Ambler (1926) made that legal at the federal level. The same year, Corrigan v. Buckley blessed racial covenants in private deeds. Then the Federal Housing Administration, starting in 1934, redlined Black neighborhoods out of the mortgage-insurance program — the regulations literally written by the chief economist of the National Association of Real Estate Boards (Richard Rothstein, The Color of Law, is the long version). Today, roughly 75% of residential land in American cities is zoned single-family only (Brookings; range is 15% in New York to 94% in San Jose). That engineered scarcity is the lock.

The debt lock got built later. Federal student loans were dischargeable in bankruptcy until 1976. By 2005 they essentially weren’t, public or private. Part 8 covered the lobbying that did that. What’s worth noticing is the pattern: three different industries, three different decades, same kind of fight, same kind of result.

I want to be careful here. Nobody is sitting in a room coordinating this. No conspiracy is required, and reaching for one is how you lose the argument. What’s required is concentrated financial interests with sustained political access, doing what concentrated financial interests with sustained political access do. The pattern is just what falls out the other side.

The Deliverable Is Compliance

So what does total immobility actually produce? Look at the numbers nobody on a Q3 earnings call has any interest in explaining.

Productivity in the United States has risen roughly 60% since 1979. Median worker compensation over the same period has risen about a sixth of that. (Economic Policy Institute has tracked this for decades; the exact gap depends on which compensation measure you use, but no honest version of the data has the two lines tracking.) Union density was 33% in the mid-1950s. It’s around 10% now, and most of what’s left is in the public sector, where workers can strike without losing their healthcare.

This is what a workforce that can’t leave looks like. You can’t walk out when walking out means a $7,000 medical bill and a missed mortgage payment. You can’t negotiate when leaving means your kid loses her pediatrician mid-treatment. You can’t start the competing business, because the runway you’d need to survive without an employer’s insurance is longer than the savings you actually have. You can’t strike. You can do the work and take what’s offered.

That’s the deliverable. The rents and the premiums and the loan servicing fees are the revenue line. The product is the labor force that can’t bargain. Wage growth that doesn’t track productivity. A union movement that hasn’t recovered from the seventies. An entrepreneurship rate that runs lower than several European peers. None of those are unfortunate side effects of three unrelated policy failures. They are what the system was for.

Forced Versus Chosen

A few honest qualifications before the closer, because the strongest version of an argument is the one that doesn’t pretend the counter-arguments aren’t there.

Not all immobility is bad. Plenty of people don’t want to leave their jobs, their cities, or their houses. Family ties, community investment, place attachment — those are real, and the argument here isn’t that mobility is a virtue and staying put is a failure. People who stay where they are because they want to stay where they are are doing fine.

Plenty of homeowners genuinely benefit from single-family zoning. Their property values are real, and the people holding those property values are not all hedge funds. Pretending otherwise is the kind of thing that loses zoning-reform votes in city council meetings every year.

Universal healthcare has real fiscal tradeoffs, covered in Part 5. Debt forgiveness has real distributional questions, covered in Part 8. I’m not relitigating any of that here.

The argument is narrower than mobility-good-immobility-bad. The argument is that the system removes the choice. Forced staying is a different thing from chosen staying, even when from a distance they look the same.

What They’re Paying For

Part 8 closed on a line: somebody is getting paid. That’s the through-line of this series and I’m not done with it. But the synthesis adds something none of the individual posts have said yet.

What they’re paying for is the immobility itself.

The insurance premium is not the product. The rent check is not the product. The student loan payment is not the product. Those are the revenue. The product is the worker who can’t leave, the entrepreneur who can’t start, the negotiator who can’t walk away. Three locks on one door, and the door is the only thing that matters.

The Fixes Are Boring

None of what follows is radical. Most of it is what other developed countries already do — or what we ourselves did, or tried to do, before the relevant industry got concentrated enough to lobby the answer out of the political mainstream. The reason these solutions sound impossible is because the people who profit from the current arrangement have spent decades and a great deal of money making sure they sound impossible. They aren’t. Three locks. The keys are well understood.

- Universal healthcare. Single-payer, Medicare for All, whatever name lands politically — the structural answer is the same one almost every other developed country reached fifty or eighty years ago. The U.S. already spends more per capita than countries with universal coverage and gets measurably worse outcomes by every indicator that isn’t “number of MRI machines per square mile.” The cost argument is wrong on its face. The opposition isn’t fiscal; it’s insurance companies and large employers protecting the leverage that employer-based insurance gives them over their workforces. That is the lock. Universal coverage is the key. There is no smaller version that works — every “compromise” iteration (the ACA, employer mandates, individual tax credits, public-option carve-outs) leaves the lock intact by design.

- Cancel federal student debt and restore bankruptcy treatment for what comes after. The system has been functionally broken for two decades — servicer fraud, sabotaged forgiveness programs, recalculation errors that always seem to land on the borrower’s side of the ledger. Wipe the existing federal debt. Then restore the dischargeability that existed before 1976 (federal loans) and 2005 (private loans), so the trap can’t be rebuilt the next time anyone looks away. Both, not one.

- Free public college and trade school. Tuition at four-year public universities, community colleges, and accredited trade programs, funded the way K–12 is funded. This is what most of our peer countries already do. It is also more or less what we ourselves did at the state level until tuition was privatized as a political choice in the late 1970s and 1980s. The current cost structure isn’t market gravity. It’s a policy outcome that can be reversed by a different policy.

- Universal childcare and pre-K. Fund both as public goods, the way K–12 is funded. Most of our peer countries do this. The current U.S. childcare market is what happens when you privatize a public good and pretend a market will produce a good outcome: prices that exceed what most second earners take home, providers who can’t pay their staff, and a workforce of women whose underpaid labor is the load-bearing wall of the whole system.

- Preempt exclusionary single-family zoning. Oregon (HB 2001, 2019), California (SB 9, 2021), and Minneapolis (citywide, 2020) have done versions at the state and city level. At the federal level, tie housing and infrastructure funding to zoning reform — the same lever the federal government already uses on transportation. Engineered scarcity is a policy choice. Choose a different policy and you get a different scarcity.

- Build public housing again, at scale. The last major federal public housing investment was decades ago. The existing stock has been deliberately starved of maintenance funding so that demolition would look like the rational endpoint. Build new units. Maintain the existing ones. Vienna runs the largest social housing program in Europe and has housing affordability the average American hasn’t experienced in a generation. The model exists. We’ve just chosen not to use it.

- End the mortgage interest deduction in its current form. It is the single largest housing subsidy the federal government provides, and it flows overwhelmingly to households that already own homes. The more expensive the home, the larger the subsidy. Cap it, means-test it, or sunset it, and redirect the revenue toward rental supply and assistance for the people the current system is squeezing out.

None of these are radical. None of them are untested. They are what comparable countries already do, and what we ourselves did or attempted to do before the relevant industries got concentrated enough to push the answers out of the conversation. The reason we don’t do them is that the people who profit from the current arrangement spend a lot of money making sure we don’t — and a fair amount more making sure the public conversation never reaches the actual answers in the first place.

If that frame is right, then most of what’s left in this series stops being about separate scams and starts being about the same one. The incarceration industry, coming up next, is the version of this argument that uses physical walls instead of financial ones. Most of what follows isn’t a different game. It’s the same game with the locks changed out for whichever lock is cheapest in the particular industry.

It’s worth asking, just once, who that arrangement is actually for. Because it isn’t us.

Leave a comment