Part 11 of Passing the Buck, a 15-part series on why we make less but pay more.

The ten installments before this one traced where the money goes — the categories where household spending has grown, the mechanisms by which it has grown, and the structural reasons for the growth. This one is about who collects it. The answer turns out to be more concentrated than I expected when I started this series, which is saying something, because the categories themselves are concentrated.

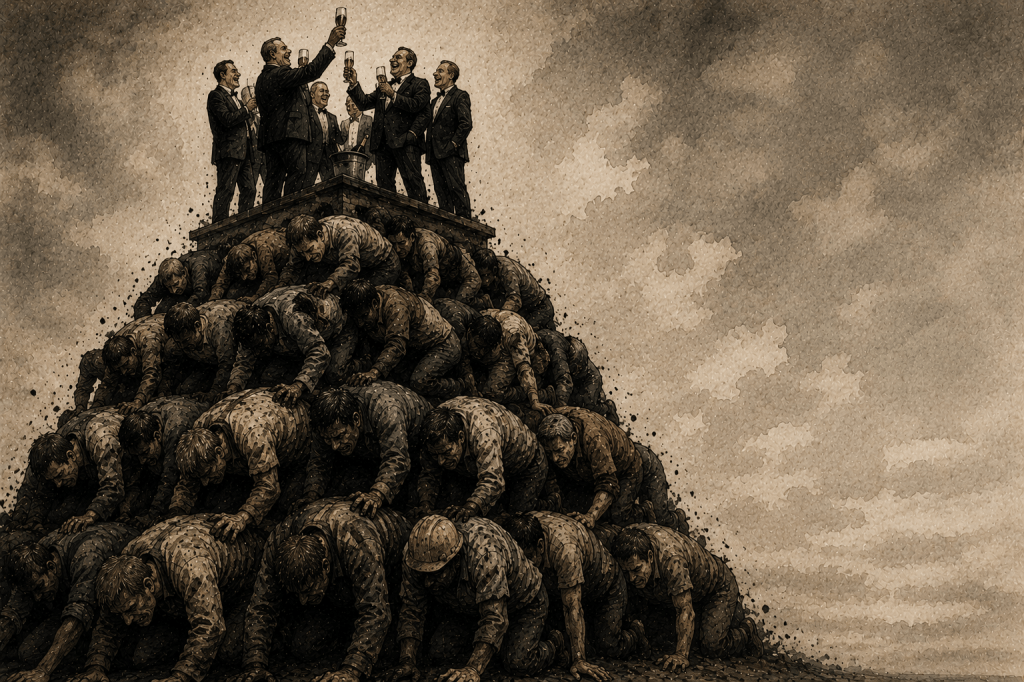

The shareholders

According to the Federal Reserve’s Distributional Financial Accounts, the most recent published quarter shows that the top one percent of U.S. households by wealth own roughly fifty-four percent of all corporate equities and mutual fund shares, up from forty percent in 2002. The top ten percent of households own ninety-three percent. The bottom fifty percent of households own about one percent of the stock market, in aggregate. These are quarterly Federal Reserve figures published from Survey of Consumer Finances microdata, not advocacy-group calculations; the numbers are as well-sourced as anything in the U.S. wealth-distribution literature. The concentration has been growing steadily for two decades and accelerated meaningfully through the post-pandemic stock market rally of 2021 through 2024.

That is the headline answer to who profits from the structural cost-shifting this series has been documenting. Corporate profits, distributed as dividends or used to repurchase shares, accrue to whoever owns the shares. Ninety-three percent of those shares are owned by ten percent of American households. The bottom half of the country, by Federal Reserve accounting, owns a rounding error.

Wage labor, which is the income source for the bottom half, has been the loser in the productivity-versus-pay decoupling that I covered in Part 1. Capital income, which is the income source disproportionately for the top, has been the winner. The mechanism that connects the two ends of that statement is exactly the cost-shifting in every installment of this series.

The Big Three

There is a more particular version of who holds the shares, and it is worth being precise about because the structural concentration here is unprecedented in modern American capital markets. Three asset-management firms — BlackRock (with roughly $11.5 trillion in assets under management), Vanguard (roughly $9.3 trillion), and State Street Global Advisors (roughly $4.3 trillion) — are now collectively the largest shareholder in approximately eighty-eight percent of S&P 500 companies. They are the largest shareholder in roughly forty percent of all publicly traded U.S. firms. They cast approximately one-quarter of all votes at S&P 500 annual shareholder meetings. Their combined assets under management equal more than half of the entire S&P 500’s market capitalization.

This is academic territory at this point, not contested by the firms themselves. The CORPNET research group at the University of Amsterdam mapped the holdings in 2017 and called the Big Three “de facto owners.” Harvard Law’s Einer Elhauge has written that concentrated common ownership “poses the greatest anticompetitive threat of our time, mainly because it is the one anticompetitive problem we are doing nothing about.” The Mason University accounting researchers Sebahattin Demirkan and Ted Polat have studied the cost-of-equity implications. The Federal Reserve’s own Distributional Financial Accounts publishes the share data quarterly. None of this is fringe.

The structural problem the Big Three pose, in plain language, is this: when a single asset manager is the largest shareholder of both Ford and General Motors, of both Coca-Cola and Pepsi, of both Verizon and AT&T, of both Bank of America and JPMorgan Chase, that asset manager has no rational economic interest in those companies competing aggressively on price against one another. The asset manager’s portfolio return is maximized when both companies in the duopoly maintain pricing power. The Harvard and University of Chicago and Yale economists who have studied this have produced a now-substantial body of empirical work suggesting that markets with high common ownership exhibit higher prices and lower output than markets without it. The mechanism is not collusion in the legal sense, which would be illegal. It is the absence of competitive pressure, which is not illegal and which the Big Three’s voting and engagement practices, by their own published statements, do little to counteract.

The Big Three themselves are not malevolent. They are doing what their charters say they should do: provide low-cost index exposure to investors. The investors are, in part, ordinary 401(k) holders, which is the appealing version of the story. They are also, much more substantively, the wealthy households who hold the bulk of all stock and therefore the bulk of all Big Three customer assets. The structural effect is the same regardless of intent. The Big Three vote with management approximately ninety percent of the time, by their own disclosure. They are, in the aggregate, the most powerful institutional voice in U.S. corporate governance, and they vote consistently for the status quo.

The flows

The numerical case is easy to assemble from public filings. S&P 500 companies in 2024 generated approximately $1.8 trillion in net income. They returned roughly $1.4 trillion of that to shareholders — about $590 billion in dividends and roughly $820 billion in stock buybacks. The buybacks alone are a category that did not exist at this scale before SEC Rule 10b-18 effectively legalized them in 1982; for most of the postwar period, what is now the dominant use of corporate free cash flow was prohibited as market manipulation.

Take that $1.4 trillion in returned capital and distribute it according to the Federal Reserve’s stock ownership data. Approximately $750 billion flowed to the top one percent of households. Another $550 billion or so flowed to the next nine percent. Less than $100 billion flowed to the bottom ninety percent combined. The aggregate transfer over a single year is larger than the GDP of all but a handful of countries.

That is the flow side of the cost-shifting. The household pays the higher cable bill, the higher insurance premium, the higher credit card interest, the higher resort fee, the higher car payment, and the higher grocery bill. The corporation that collects each of those payments is in a more concentrated market than it was thirty years ago, and it returns a larger share of the resulting profit to shareholders than it did thirty years ago, and the shareholders are concentrated more than they were thirty years ago. Every step of the chain has gotten more extractive at the same time.

CEOs and the rest of the executive class

The executive compensation story sits on top of the shareholder story rather than being separate from it. Average CEO compensation for S&P 500 companies, per the Economic Policy Institute’s tracking, runs around $16-17 million per year, against average non-supervisory worker compensation of roughly $66,000. The ratio is now 344 to 1. In 1965 it was 21 to 1. In 1989 it was 61 to 1.

Most of the dollar magnitude in modern executive compensation is stock-based: restricted stock awards, performance shares, stock options. That is not a coincidence. The structure ties the executive class’s interests to the shareholder class’s interests rather than to the worker class’s interests, and the structure is by design. When a CEO chooses how to allocate free cash flow — between wages and capital investment on the one hand, and dividends and buybacks on the other — the CEO’s own compensation package is structured to reward the second choice. The dividends-and-buybacks share of cash flow has grown over forty years, and the wage-and-capital-investment share has shrunk, for reasons that include but are not limited to this.

The names of the highest-paid CEOs are familiar from previous installments. Mike Sievert at T-Mobile (~$30 million in 2024, more in earlier years). Brian Roberts at Comcast (low-to-mid $30 million range and family ownership of a third of Comcast’s equity worth tens of billions). Jamie Dimon at JPMorgan Chase (mid-$30 million range, with a $1.8 billion personal Chase stake). Andrew Witty at UnitedHealth (mid-$20 million range, until his role transitioned in the aftermath of last December). The aggregated pay of the S&P 500 chief executive class is, on its own, a number in the single-digit billions of dollars per year — small in the context of the overall trillion-dollar shareholder distribution flow, but symbolically large, and culturally large, and large enough to fund the lobbying-and-political-influence apparatus that protects everything else.

The political-influence apparatus

The corporate sectors that recur through this series — banking, insurance, telecommunications, pharmaceuticals, energy — are also the sectors that dominate the federal lobbying registry. According to OpenSecrets, the U.S. lobbying spend in 2024 was approximately $4.4 billion, with the largest individual-sector spends in the hundreds of millions. The pharmaceutical industry alone spent over $370 million. Insurance and the broader financial-services sectors spent over $600 million between them. Telecom and oil/gas were each in the nine-figure range.

Corporate PAC and trade-association political contributions are roughly evenly split between the two major parties, and have been for most of the post-Citizens-United period. That is the structural reason this series has, in the relevant installments, been even-handed across administrations: the Obama-era CARD Act and Dodd-Frank were real consumer-protection wins that came out of one administration; the No Surprises Act and the FTC Junk Fees Rule and the Biden CFPB rules were real wins that came out of another; the credit card late fee cap was killed by a Texas court and then abandoned by the next administration’s CFPB. There is no single party of cost-shifting and no single party of consumer protection. There is a system in which both parties depend on corporate fundraising and act, at the margin, in ways that protect the underlying structure regardless of which is in power.

The revolving door between federal agencies and the industries they regulate is well-documented and bipartisan. The FCC chairmen who have made the most consequential decisions on telecommunications policy over the past fifteen years — Ajit Pai before, Jessica Rosenworcel during, Brendan Carr now — all came from industry-adjacent legal practice or industry employment, and several have returned to it. The Treasury secretaries who oversee financial regulation are almost always drawn from Goldman Sachs or its competitors and frequently return there. The pharmaceutical industry has, by various counts, more former federal employees on its payroll than active federal employees in any of the relevant agencies. The pattern is older than any current administration and will outlast any current administration.

The plain version

Stripped down, the picture is this. A small share of American households, roughly ten percent, own ninety-three percent of the country’s stock market. Three asset-management firms have become the dominant institutional voice of that ownership, holding the largest single position in nearly every major U.S. corporation. The corporations themselves have, sector by sector, consolidated into four-firm or three-firm oligopolies with the pricing power that comes with it. The household at the consuming end of all of this faces higher prices, larger fees, narrower networks, and more drip-pricing than it did a generation ago. The profits from that flow upward through the corporations to the asset managers to the wealthy households that own the asset-manager-mediated index funds. The political and regulatory apparatus, funded on both sides by the same corporations, has at the margin made it easier rather than harder for the flow to continue.

This is not a conspiracy. It is an emergent system that nobody at any single level needs to have planned for it to work the way it works. Larry Fink at BlackRock is not personally directing UnitedHealth to deny claims. Larry Fink does not need to. The system, as constructed, generates the outcome without anyone consciously coordinating to produce it. The buybacks happen because the executive compensation is structured to favor them. The compensation is structured that way because the boards approving it are populated by people drawn from the same shareholder-aligned class. The shareholders are concentrated because the wealth distribution has been allowed to concentrate over forty years of tax and labor policy that did the concentrating. The political system that could change those policies is funded by the same shareholders. The loop closes.

The good news, such as it is, is that emergent systems can be re-engineered if the political will exists. There is no need to identify a villain. The structural levers — antitrust enforcement, corporate governance rules, executive compensation structure, the tax treatment of capital income versus labor income, the post-Citizens-United campaign finance system, the SEC rules governing share repurchase — are all known, all visible, all the subject of substantial policy literatures, and all in principle changeable. The will to change them is the part this series cannot manufacture. It can only describe what is.

The next installment looks at the tax code, which is where many of the structural choices that produced the current concentration were made.

Leave a comment