Part 2: The Baseline Shift

How “Basic Survival” Got Redefined as Luxury

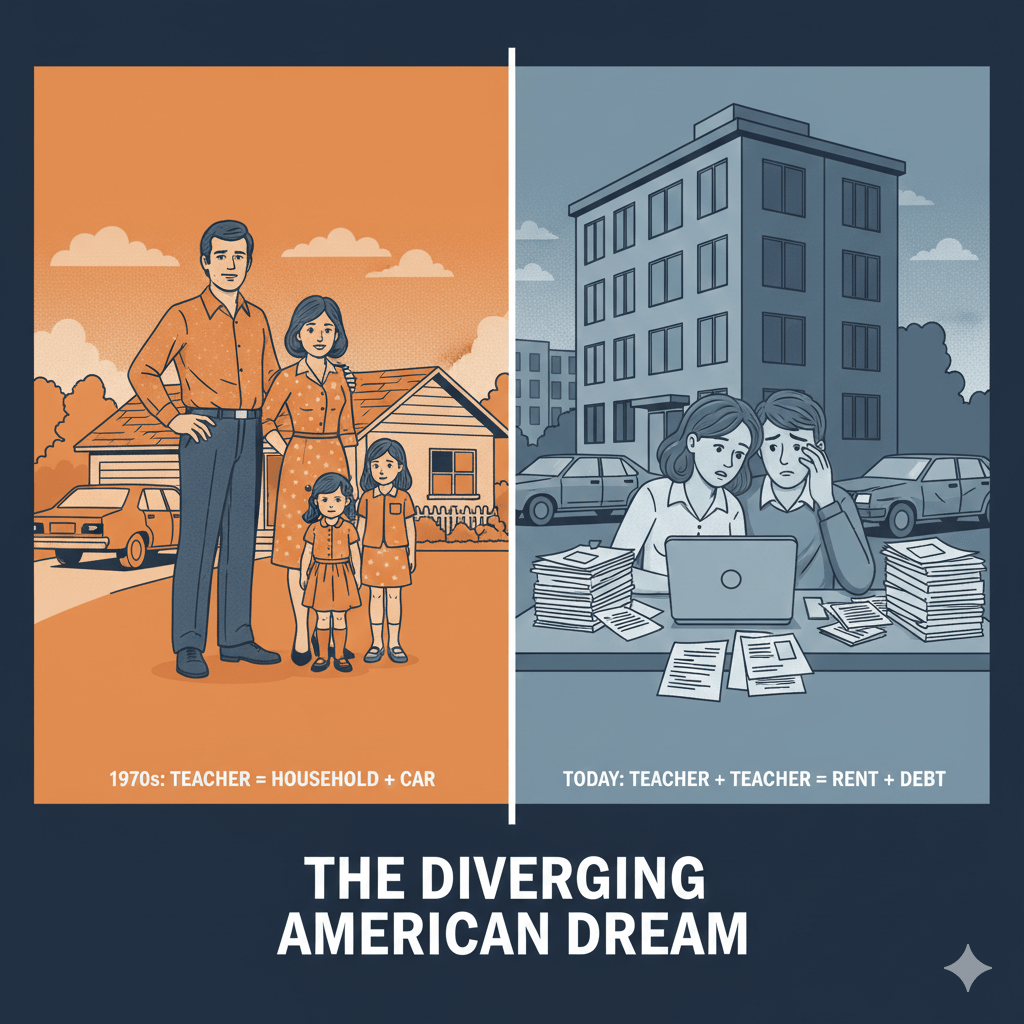

In 1970, Robert worked as a machinist at a manufacturing plant in Ohio. He made $9,400 a year—roughly the median income at the time. His wife, Linda, stayed home with their two kids.

On that single income, they:

- Owned a three-bedroom house

- Had two cars (one new, one used)

- Had full healthcare coverage with no premiums

- Sent their kids to college

- Took a week-long family vacation every summer

- Saved 10% of their income

- Had a pension waiting at retirement

Robert wasn’t exceptional. He wasn’t a high earner. He was median. And median was enough.

Today, Robert’s grandson Mike does the same kind of work—CNC machining at an auto parts supplier. Mike makes $52,000 a year, which is close to today’s median individual income of $59,228.

Mike’s wife also works, bringing in another $45,000 as a dental hygienist. Their household income is $97,000—above the median household income of $80,610.

With nearly double the income of what grandpa had (adjusted for inflation), Mike and his wife:

- Rent a two-bedroom apartment (can’t afford to buy)

- Have two used cars with loans

- Pay $600/month for health insurance with a $6,000 family deductible

- Have $47,000 in student loans between them

- Haven’t taken a real vacation in three years

- Save nothing

- Have 401(k)s they can’t afford to fund

Same work. Double the workers. Higher real income. Worse outcomes.

What the hell happened?

The Numbers Don’t Lie

Let’s compare what median income could buy in 1970 versus what it buys today.

Housing: From Achievable to Impossible

1970:

- Median home price: $23,400

- Median household income: $9,870

- Home-to-income ratio: 2.4x

- Down payment (20%): $4,680 (5.7 months of income)

- Mortgage payment: ~$185/month (22% of gross income)

2024:

- Median home price: $412,300

- Median household income: $80,610

- Home-to-income ratio: 5.1x

- Down payment (20%): $82,460 (12.3 months of income)

- Mortgage payment: ~$2,500/month (37% of gross income)

Even with two incomes today, a house costs more than double what it did when one income was the norm. The 20% down payment alone would take a median household over a year of saving every penny—and that’s before taxes, food, or rent while saving.

In 1970, if you saved 10% of your income, you’d have that down payment in under 5 years while covering all your other expenses. Today, saving 10% would take 10 years just for the down payment—assuming home prices don’t increase (they will) and you can actually save that 10% (most can’t).

Healthcare: From Covered to Crushing

1970:

- Average healthcare spending: $356 per person per year

- Most employer plans: 100% employer-paid, no deductibles

- Out-of-pocket costs: minimal

- Percentage of income: ~3.6%

2024:

- Average healthcare spending: $14,570 per person per year

- Typical employer plan: Employee pays $6,575/year for family coverage

- Average family deductible: $4,200

- Out-of-pocket max: Often $8,000-$16,000

- Percentage of median household income: ~18%

Healthcare costs have increased 4,092% since 1970, while median wages increased just 17% (inflation-adjusted).

But here’s the kicker: In 1970, your employer paid for healthcare as part of your compensation package. It was considered basic—like paying you in money rather than chickens. Today, if your employer covers 80% of premiums, they act like they’re doing you a favor.

Your grandfather paid $0 in premiums and had no deductible. You pay $6,575 in premiums before you can use your insurance, then hit a $4,200 deductible, then still pay 20% coinsurance up to your out-of-pocket maximum.

Same healthcare. You just pay for it now instead of your employer.

Education: From Affordable to Debt Sentence

1970:

- Average public university tuition: $394/year

- Median income: $9,870

- Percentage of income: 4%

- Students working part-time could pay tuition

- Average student debt at graduation: $1,070 (equivalent to $8,200 today)

2024:

- Average public university tuition: $27,940/year (in-state)

- Median income: $59,228 (individual)

- Percentage of income: 47%

- Students working full-time can’t pay tuition

- Average student debt at graduation: $40,681

In 1970, you could work a summer job and pay for a year of college. A student making minimum wage ($1.60/hour) working 40 hours a week for 12 weeks earned $768—nearly double the annual tuition.

Today, a student making minimum wage (federal $7.25, let’s be generous and say $15/hour in a decent state) working 40 hours a week for 12 weeks earns $7,200—barely a quarter of annual tuition.

A 1970 student could graduate debt-free by working summers. A 2024 student can work full-time year-round and still need loans.

College hasn’t gotten 70 times better. It got 70 times more expensive because:

- State funding was slashed (shifted to students)

- Federal loans expanded (schools raised prices knowing students could borrow)

- Administrative costs exploded (students pay for bloat)

The cost shifted from society investing in its workforce to individuals going into debt for the privilege of being employable.

Transportation: From Months to Years

1970:

- Average new car price: $3,542

- Median income: $9,870

- Months of income: 4.3

- Cars lasted ~100,000 miles with maintenance

2024:

- Average new car price: $48,759

- Median income: $59,228

- Months of income: 9.9

- Cars last ~200,000 miles with maintenance

Cars have gotten better—they last twice as long. But they cost twice as many months of salary, so you’re not actually ahead. And now you’re more car-dependent because:

- Public transportation was defunded

- Cities sprawled (cheap housing is far from jobs)

- Zoning separated residential from commercial (must drive everywhere)

In 1970, more cities had functional public transit. Today, 45% of Americans have no access to public transportation whatsoever. A car isn’t a luxury—it’s mandatory. And mandatory things shouldn’t cost 10 months of gross income.

The Wage Stagnation Context

All these costs would be manageable if wages had kept pace with productivity gains. They didn’t.

Productivity vs. Wages Since 1970:

- Worker productivity: Up 77%

- Hourly compensation: Up 17% (inflation-adjusted)

If wages had tracked productivity—as they did from 1948 to 1973—the median worker would make approximately $102,000 today instead of $59,228.

Let that sink in. You produce 77% more value per hour than your parents did in 1970. You’re paid for 17% more.

Where did the other 60% go?

Corporate Profits:

- 1970: Corporate profits were 4.3% of GDP

- 2024: Corporate profits are 11.1% of GDP

Executive Pay:

- 1965: CEOs made 21x the average worker

- 2023: CEOs make 344x the average worker

Shareholder Returns:

- Total shareholder returns have increased 5-fold since 1970 (adjusted for inflation)

That 60% productivity gain that you didn’t get? It went to shareholders, executives, and corporate profits. You made them richer by being more productive. They thanked you by stagnating your wages while shifting costs onto you.

What We Lost: The Redefinition of “Basic”

Here’s what was considered standard and expected in 1970:

Employer-Paid Healthcare

In 1970, employer-paid healthcare was normal. You got hired, you got healthcare, no premiums. It was as basic as getting a paycheck.

Today, if your employer covers 80% of premiums, they market it as a “competitive benefits package.” The cost shifted from employer to employee, but the messaging shifted too: from “this is basic compensation” to “you should be grateful we chip in.”

Pension Plans

In 1970, 45% of private-sector workers had a defined-benefit pension. Your employer promised you a specific monthly income in retirement based on your salary and years of service. You worked, they set aside money, you retired with security.

Today, only 14% of private-sector workers have a pension. Instead, you get a 401(k)—which means:

- You fund it (not your employer)

- You manage it (not finance professionals)

- You bear the risk (market crashes hit your retirement)

- You die with whatever’s left (no guaranteed income)

The shift from “we’ll take care of you in retirement” to “figure it out yourself” was a massive cost transfer. Companies saved billions. You now carry the burden and risk.

One-Income Families

In 1970, 40% of families had a stay-at-home parent. This wasn’t “luxury”—it was normal. One income was enough.

Today, 27% of families have a stay-at-home parent, and most of those are higher-income families. For median-income families, one income won’t cover basics.

The shift wasn’t that people decided they’d rather both work. The shift was that wages stopped covering survival. Two-income became mandatory, not optional. But:

- Childcare now costs $1,700/month (national average)

- Which is often more than the second income nets after taxes

- But you still need two incomes because one won’t cover rent and health insurance

Paid Time Off

1970 Standard:

- 2 weeks paid vacation (often 3 after 5 years)

- Unlimited sick days (or at least 10-15)

- Paid holidays (8-10 per year)

2024 Reality:

- 11 days average vacation (after 1 year)

- 8 days average sick leave

- Many jobs combine PTO (use vacation days when you’re sick)

- 25% of workers have no paid leave at all

Taking time off used to be expected—your employer understood humans need rest. Today, using your PTO is seen as letting down the team.

Job Security

In 1970, if you did good work, you kept your job. Layoffs happened during recessions, not during record profit years to boost stock prices.

Today:

- “At-will” employment means no cause needed to fire you

- Mass layoffs happen to hit quarterly targets

- “Right-sizing” and “efficiency gains” mean you’re disposable

- Non-compete clauses (even for low-wage workers) trap you

The Messaging Shift: From “Basic” to “Entitled”

Here’s the insidious part: They didn’t just shift the costs. They shifted the narrative.

When your grandparents expected employer-paid healthcare, they weren’t “entitled.” That was the deal. You work, we provide healthcare. Basic compensation.

Now, if you expect healthcare, you’re “entitled.” You should be “grateful” for “benefits.” The language itself shifted to make you feel like you’re asking for something extra when you’re actually asking for what used to be standard.

What used to be normal:

- Single income supporting a family → Now: “Unrealistic expectations”

- Employer-paid healthcare → Now: “Premium benefits”

- Pension security → Now: “Government employee privilege”

- Affordable education → Now: “Subsidizing lazy kids”

- Work-life balance → Now: “Not a team player”

They convinced you that wanting what your grandparents had is entitled. That expecting productivity gains to be shared is greedy. That thinking one full-time job should cover basics is naive.

Meanwhile, corporate profits tripled, executive pay increased 16-fold, and shareholder returns soared.

They took your productivity gains. They shifted their costs onto you. And they convinced you that YOU’RE the problem for expecting what used to be normal.

The Result

Robert, the machinist from 1970, built a middle-class life on one median income. House, cars, healthcare, education, retirement, savings.

Mike, his grandson doing the same work today, can’t build that life on two median incomes.

It’s not because Mike is less hardworking. It’s not because he’s bad with money. It’s not because he wants too much.

It’s because:

- Housing costs doubled (as a multiple of income)

- Healthcare shifted from employer-paid to self-funded

- Education went from affordable to debt sentence

- Pensions became 401(k)s (your risk, your money)

- Wages stagnated while productivity soared

- All the costs went down, none of the gains came back

Your grandparents weren’t smarter than you. They weren’t more disciplined. They didn’t “just work harder.”

The math was different.

And the people who changed that math got obscenely wealthy while convincing you that expecting what used to be normal makes you entitled.

What’s Next

In Part 1, we showed you the impossible math: median income doesn’t cover basic costs anymore.

Now you know why: decades of cost-shifting while wages stagnated and benefits disappeared.

Starting in Part 3, we’re going to examine each shift in detail. We’re going to show you exactly how much was extracted, who collected it, and how they convinced you it was normal.

We’re starting with banking fees—a $34 billion annual extraction from the people who can least afford it. Because the shift wasn’t just from employer to employee. It was from those with resources to those without them.

They don’t just take from workers. They take most from the poorest workers.

And it’s time you saw exactly how.

Passing the Buck: Why We Pay More But Make Less is a 15-part series examining how corporations and government systematically shifted costs onto working Americans—while wages stagnated and benefits disappeared.

Leave a comment