Part 2 of Passing the Buck, a 15-part series on why we make less but pay more.

In Part 1 I walked through the math on one specific case — a nurse making $77,000 a year, doing everything right, with $625 a month left after mandatory expenses. The argument was that the math has gotten harder. This installment is about how much harder, and what changed underneath to make it that way.

I want to do this through comparison, because comparison is what actually shows you the shape of the thing. Numbers in isolation are just numbers. Numbers next to other numbers from another era — when the same kind of person, doing the same kind of work, lived a different kind of life — start to mean something.

So: 1970 versus 2024.

Housing

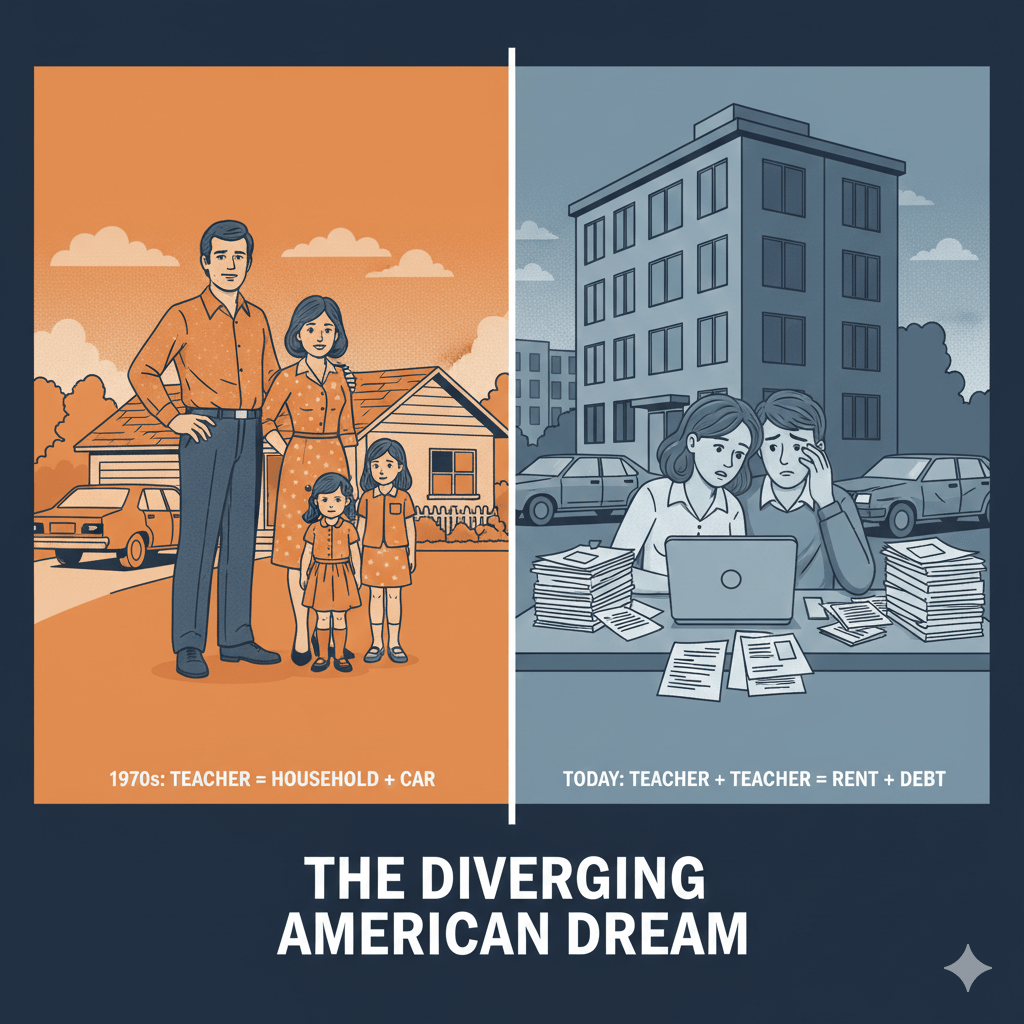

In 1970, the median home in the United States cost about $23,400. The median household income was about $9,870. That is a house-to-income ratio of 2.4. A regular working family could buy a regular working family’s house using a little over two years of regular working family income.

In 2024, the median home cost about $412,000. The median household income was about $80,600. That is a house-to-income ratio of about 5.1. Roughly double. And that is at the national median — in any major metro area, or any desirable smaller market like the one I live in, the ratio is meaningfully higher. In parts of the Hudson Valley a young couple looking at a tear-down is looking at six or seven times household income before they have replaced a single window.

The 20% down payment that used to take a family about half a year of saving now takes about a year of household income, assuming the family can save a hundred percent of their income, which obviously nobody can. The mortgage payment that used to be twenty-two percent of gross income is now closer to thirty-seven percent on the same kind of house, before property taxes and insurance, which have also grown faster than wages.

The house got the same number of rooms. The math doubled.

Healthcare

In 1970, the United States spent about $356 per person per year on healthcare, across the whole system. In 2024 that number was around $14,500 — about forty times higher in nominal dollars, and roughly seven times higher even after inflation. Healthcare did not get seven times better. People do not live seven times longer or get sick seven times less often. The cost went up. The outcomes did not.

And the cost did not just go up. It moved. In 1970, most workers at a steady employer paid no premium and had no deductible. Healthcare was part of compensation, the same way wages were. Today the average family covered by an employer plan pays about $6,500 a year in premiums for that coverage, faces a deductible somewhere north of $4,000 before the plan starts paying for routine care, and can be on the hook for fifteen thousand-plus before the year is done if something serious happens. The cost did not just go up. It shifted from the employer’s books to the household’s books, and the conversation around it shifted with the cost. What used to be base compensation is now called a “benefit,” as if the employer is doing you a favor by providing what used to be standard.

Higher education

In 1970, in-state tuition at the average public four-year university ran about $400 a year. In 2024 it was about $11,600 — a thirty-fold nominal increase, or about a six-fold real increase after inflation. A student in 1970 could earn the price of a year of tuition in a summer of minimum-wage work. A student today cannot earn the price of a year of tuition working full-time at federal minimum wage all summer. The summer job that used to pay for school now does not even pay for the books.

The reason it changed is that the cost shifted. Until the late 1970s, state legislatures funded public universities directly as part of the public investment that produced the workforce. As that public funding was cut — over decades, in both red and blue states, though faster in red ones — the cost moved onto the student. Federal loans expanded to fill the gap, which is to say the cost did not actually go away. It just changed pockets, from the taxpayer’s to the borrower’s, with interest.

Cars

In 1970, the average new car cost about $3,500. In 2024 it was about $48,000. As a fraction of median income, that is roughly twice as expensive. Cars have gotten meaningfully better — they last twice as long, on average — but they cost twice as many months of work to buy, and the country has been designed in the intervening fifty-five years to make a car much more mandatory than it used to be. Public transit funding shrank. Suburbs sprawled. Zoning separated where people sleep from where they work and shop. In huge stretches of the country, no car means no job.

Pensions

This is the one I watched happen during my own working life. In 1970, somewhere in the neighborhood of forty percent of private-sector workers had a defined-benefit pension — an actual promise from their employer, backed by the employer’s actual books, of a specific monthly amount in retirement based on what they earned and how long they worked. Today that number is closer to fourteen percent and still falling.

I was inside one of those transitions. In broadcast television in the late 1990s and early 2000s, the union pensions that had backed my older colleagues’ retirements were being frozen, closed to new hires, and replaced with 401(k)s. Each change was rolled out internally as “modernization,” and what it actually meant was that the financial risk of getting old was moving from the company’s balance sheet onto each individual employee’s shoulders, while the company’s contribution shrank. The senior people I worked with under the old system retired into a guaranteed monthly check. The people who came up under the new system get whatever they remembered to put aside, in a market that may or may not be cooperative the year they need to draw on it.

The math of that shift is enormous. A pension is an obligation the employer carries. A 401(k) is a savings vehicle the employee funds. Same employee, same work, same retirement. The cost did not go away. It moved.

Where the money went

When a society’s productivity rises and the share that goes to the people doing the work falls, the share has to be going somewhere else. That is just accounting.

EPI’s analysis of CEO compensation puts the ratio of CEO pay to typical worker pay at about 21 to 1 in 1965 and about 344 to 1 by 2022. Top-quintile earners as a share of national income are at levels not seen since before the Second World War. Corporate profits as a share of GDP have roughly doubled since 1970, from around five percent to over eleven. The shares granted in stock-based executive compensation, and the buybacks that have absorbed roughly a trillion dollars a year of corporate cash for most of the last decade — that is not money that vanished into the ether. That is the productivity gap, paid in a different form to a different group of people.

This is not a conspiracy. It is the visible record of forty-five years of policy choice — tax law, labor law, antitrust enforcement, public investment, the legal status of unions and shareholders relative to each other. Every one of those changes has names and dates attached to it. Most of the remaining installments in this series will name some of them.

What we lost vocabulary for

The other thing that happened, alongside the money moving, is that the language around the deal changed.

When my parents’ generation expected employer-paid healthcare, they were not “entitled.” They were paid in the way employees of stable companies had been paid for a generation, which included paying their medical bills. When they expected a pension, they were not asking for a handout. They were referring to the deferred-compensation contract their employer had with them. When they expected a job to last for a couple of decades if the work was good, they were not naive. Stable employment was a normal feature of the kind of employer most of them worked for.

Today, anyone who expects any of those things is told they are out of touch with how things actually work. The relationship has been redefined to make the thing your parents had look like a luxury, and you look unreasonable for wanting it. None of the underlying productivity disappeared. None of the underlying wealth disappeared. The wealth grew. The arrangement just changed who gets to keep it.

I am not trying to be nostalgic about 1970. Half the people in my life would not have been allowed full participation in the 1970 deal even if they wanted it. But the 1970 deal was the floor under the middle class for a generation, and the structural change since then has been to lift the floor away while keeping the language of personal responsibility in place. If you cannot afford a house on a normal job, the problem is presented as yours: you should have made better choices, gotten a better degree, picked a better field, saved harder. The math does not get questioned.

The math is what changed. The rest of the series is about how it changed, one cost at a time.

Leave a comment